Addressing the Paytm Issue with RBI: Ensuring Compliance at Skydo

The Reserve Bank of India (RBI) serves as the supreme authority overseeing and regulating India's money market. RBI imposes penalties on banks and Non-Banking Financial Companies (NBFCs) for failing to comply with prescribed frameworks and guidelines, implementing necessary restrictions when required.

A significant recent operational restriction imposed by RBI was on Paytm Payments Bank. This blog aims to provide insights into the Paytm Payments Bank RBI ban and explore strategies for ensuring better compliance moving forward. Join us to understand this important development and its implications.

What Went Wrong With Paytm?

It was all smooth sailing for Paytm and its subsidiary, Paytm Payments Banks, until January 31st when the RBI announced that it had placed major restrictions on the NBFC. The RBI was exercising its right under Section 35A of the Banking Regulation Act of 1949, to issue directives to banks and NBFCs to protect their customers’ financial interests.

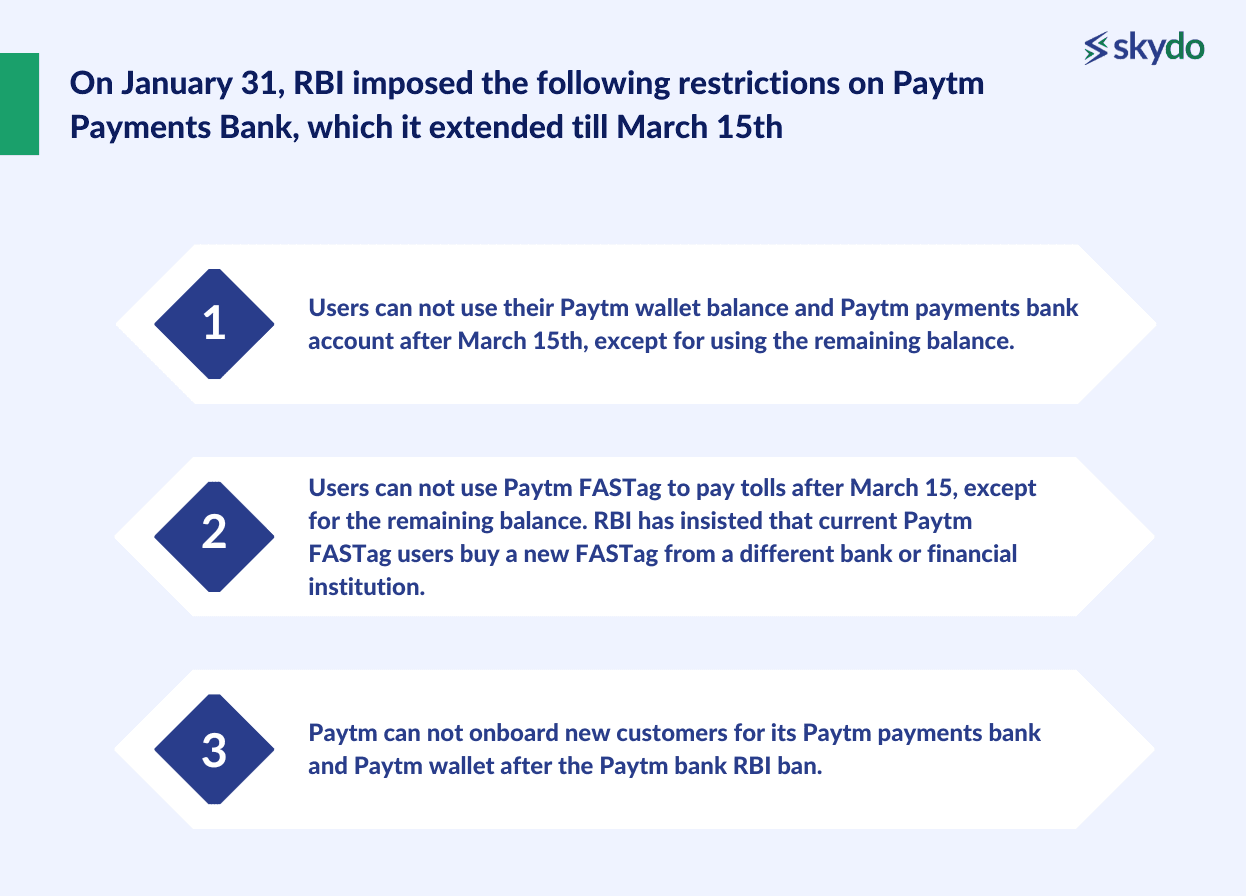

On January 31, RBI imposed the following restrictions on Paytm Payments Bank, which it extended till March 15th.

- Users can not use their Paytm wallet balance and Paytm Payments Bank account after March 15th, except for using the remaining balance.

- Users can not use Paytm FASTag to pay tolls after March 15, except for the remaining balance. RBI has insisted that current Paytm FASTag users buy a new FASTag from a different bank or financial institution.

- Paytm can not onboard new customers for its Paytm Payments Bank and Paytm wallet after the Paytm bank RBI ban.

Why Did RBI Put Restrictions on Paytm?

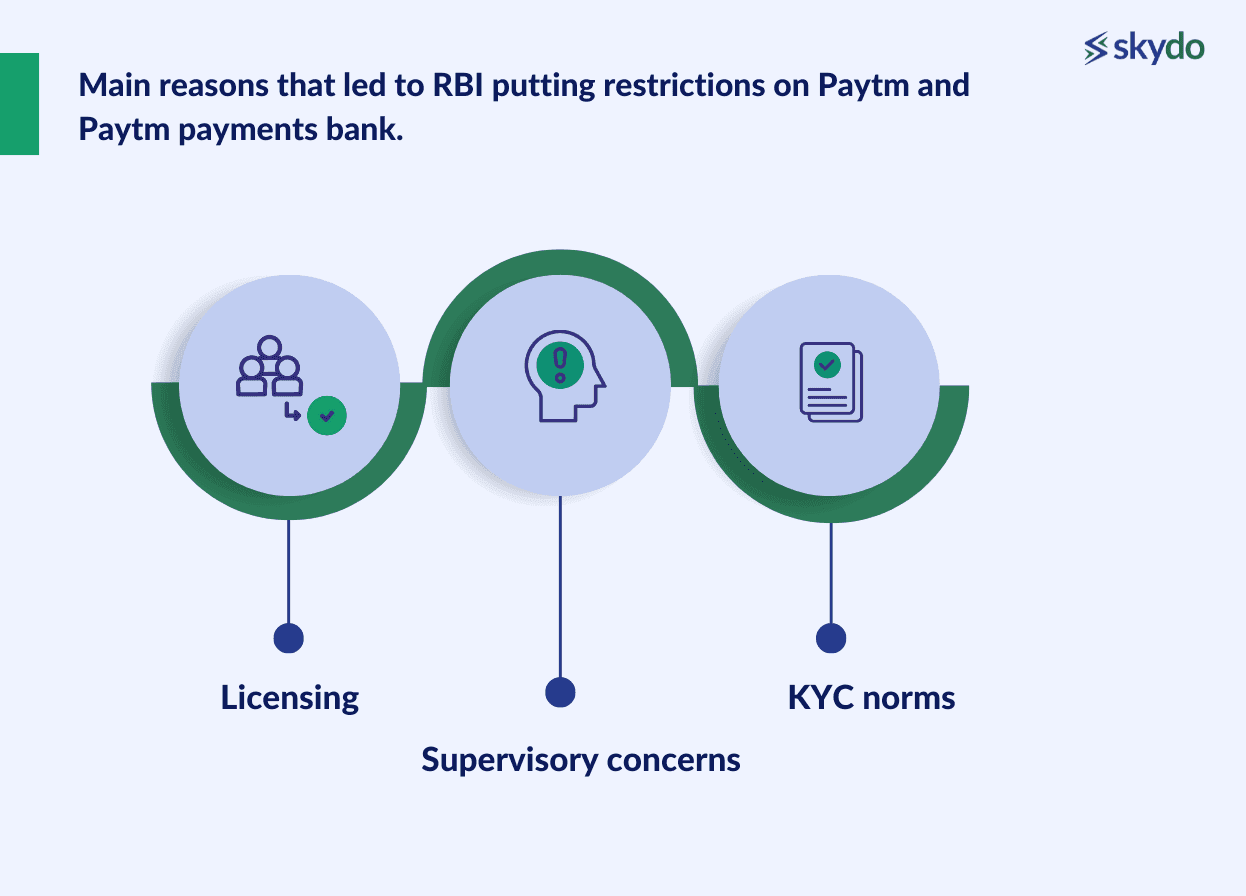

Here are the main reasons that led to RBI putting restrictions on Paytm and Paytm Payments Bank.

Licensing

Under RBI’s guidelines for payment banks, they can not undertake lending activities. However, RBI identified that although Paytm Payments Bank does not lend to customers directly, it indirectly provides third-party credit-dispensing products.

One example is when you apply for loans from Paytm’s platform, they do not provide the loan directly but offer credit-dispensing products from top NBFCs.

Supervisory Concerns

Paytm owns 49% of Paytm Payments Bank, and the remaining 51% is owned by its founder and CEO, Vijay Shekhar Sharma. Although founders and parent entities can own a business, RBI requires the operations to be run independently by the company management to ensure they are aligned with customer interests.

RBI noted that although Paytm has maintained that the bank is run independently without any external influence, the governance has been highly influenced by Paytm and its CEO.

KYC Norms

Thousands of bank accounts were identified to have been linked with a single PAN. RBI noted that if multiple fake accounts are created without the PAN holder's knowledge, the intention must be to use them for laundering money because it is difficult to identify the beneficial owner in such cases.

Furthermore, it drastically eroded the trust of users and seriously jeopardised the operational and security protocols needed for regulatory compliance.

What Now For Paytm?

Paytm and its founder and CEO Vijay Shekhar Sharma have announced that they are in frequent touch with RBI and holding talks to determine the next course of action to ensure the lifting of Paytm bank RBI ban. In an official response, Paytm announced that the ban would hurt its annual earnings by a staggering ₹300 crore to ₹500 crore. Meanwhile, Paytm Payments Bank has paused its primary services, such as credit and deposit transactions, FASTag services, and onboarding of new customers.

Best Compliance Practices For Fintechs in India

The fintech segment in India has to comply with extensive regulatory and supervisory compliance requirements from various authorities such as the RBI and SEBI. Similar to Paytm, there are over 3,000 fintech firms in India.

However, to ensure that they don’t experience the same restrictions as Paytm, here are some of the best compliance practices to consider.

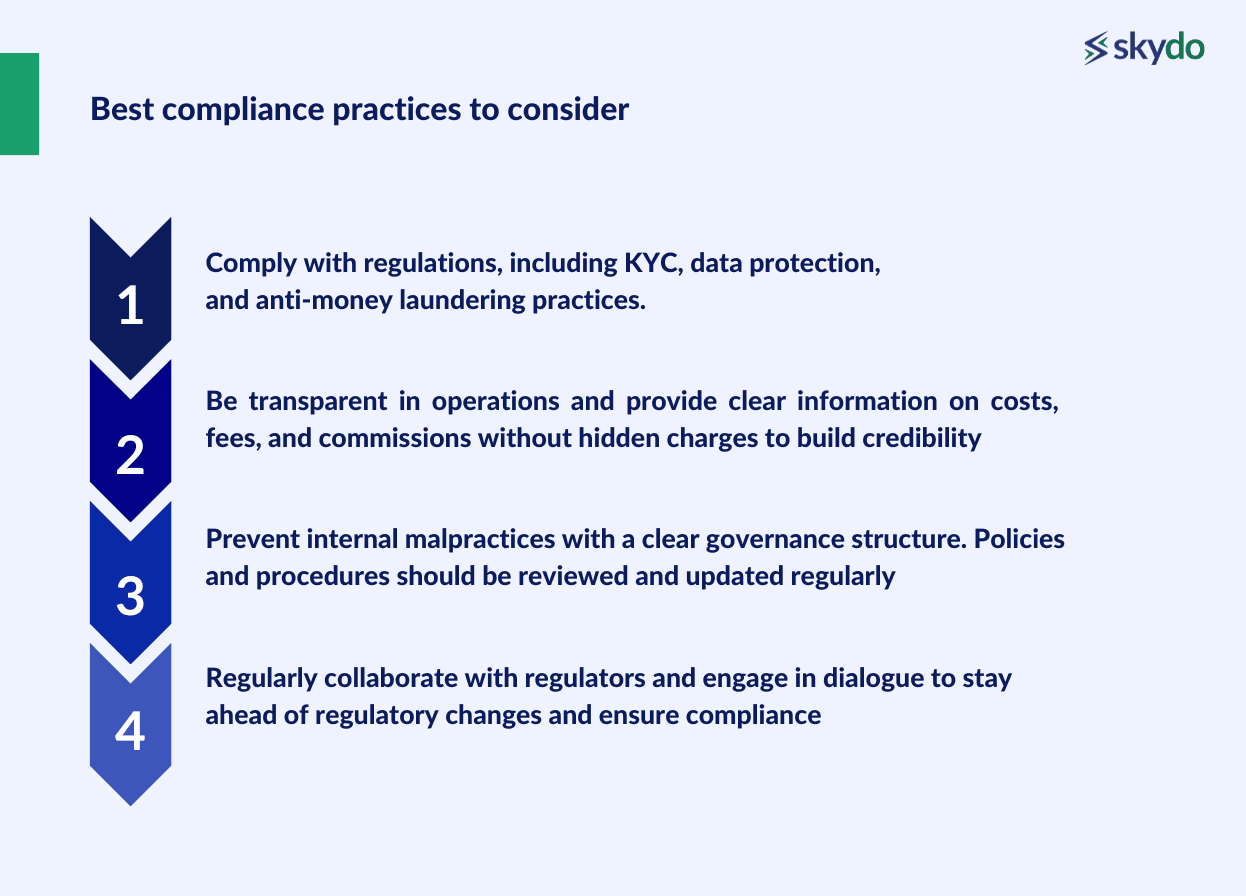

- Fintechs must ensure effective regulatory compliance, including robust KYC norms under Master Direction - Know Your Customer (KYC) Direction, 2016, compliance with data protection laws, and adherence to anti-money laundering practices.

- Fintechs must provide transparency in their operations and financial transactions. This includes providing clear information about the cost structure, commissions or fees for every service without hidden charges to build credibility.

- Establishing a detailed organisational governance structure with defined authority, roles and responsibilities is also beneficial to prevent internal malpractices. The management must constantly review and update governance policies and procedures.

- It must regularly collaborate with regulators and engage in dialogue to stay ahead of regulatory changes and ensure compliance.

- All Authorised Payment System Operators (PSOs) must also comply with RBI’s Storage of Payment System Data direction. As per this, PSOs are required to store all data related to payment systems in India.

- PSOs should also adhere to RBI’s Information Technology Framework for the NBFC sector. This framework provides directions on IT governance, infrastructure and services management, information security risk management, audit and cybersecurity.

Since the Paytm Payments bank, customers and merchants have been forced to look at alternatives. However, the platform or institution they choose must have ideal policies and frameworks to ensure seamless RBI compliance.

Similarly, with international payments, you need a platform that complies with RBI guidelines to ensure you receive payouts smoothly. Skydo is one such platform that facilitates international payments while staying true to all RBI regulations. Here’s how it works.

How Skydo Ensures Seamless RBI Compliance?

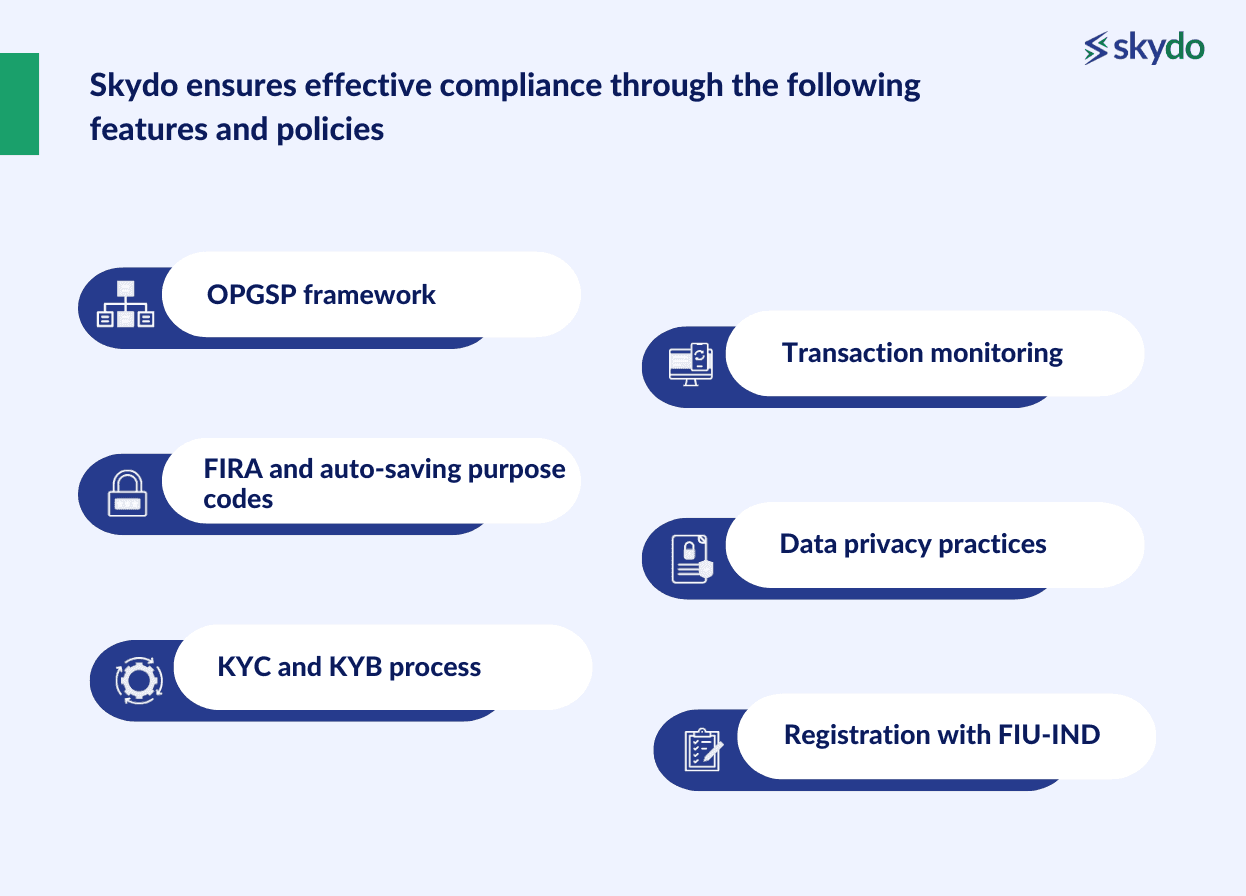

Skydo ensures effective compliance through the following features and policies.

OPGSP Framework

Skydo ensures effective compliance with industry regulations as it follows guidelines set by the Reserve Bank of India (RBI) under the OPGSP framework. RBI has set guidelines related to Online Payment Gateway Service Providers (OPGSPs) and their arrangements with Authorised Dealer (Category I) Banks.

Skydo constantly monitors the RBI framework to regulate its operations and ensure it follows the RBI’s OPGSP guidelines.

FIRA and Auto-saving Purpose Codes

A Foreign Inward Remittance Advice (FIRA) is a document issued by Indian banks to Indian beneficiaries who receive foreign remittances into their bank accounts. Skydo offers Automated Digital FIRA, where the document is automatically generated immediately when you receive foreign funds in your virtual Skydo account. This saves time and ensures you are GST-compliant with every completed transaction.

Furthermore, when you execute an international transaction on Skydo, your purpose codes are automatically saved and seamlessly integrated into your invoices. This allows effective regulatory compliance, risk management, and transaction transparency.

KYC and KYB Process

For financial platforms and institutions, adequate KYC (Know Your Customers) and KYB (Know Your Business) processes are vital as penalties for flouting such processes by RBI are the most common.

Skydo has created detailed yet quick KYC and KYB processes to prevent money laundering, terrorist financing, and other illicit activities.

Transaction Monitoring

Skydo monitors every transaction you execute through your virtual currency account and ensures there are no unusual activities, to maintain a safe and trustworthy environment.

Data Privacy Practices

Creating an account and executing transactions leave a data trail about the sender and the receiver. Skydo ensures the safety of your money, data, and client/business information through top-grade encryption.

Skydo keeps your data in a virtual safe, with an extra layer of security access. Furthermore, Skydo follows processes aligned with the new Data Protection Act to ensure your data is handled with the utmost care and in compliance with evolving regulations.

Registration with FIU-IND

Financial Intelligence Unit - India (FIU-IND) is a national agency that receives, processes, analyses, and disseminates information relating to suspicious financial transactions. Skydo has registered with FIU-IND to report suspicious activity.

Conclusion

RBI has set guidelines and frameworks to protect customer data and money, and it should be the foremost priority of platforms and institutes to ensure their operations and processes comply with RBI guidelines.

For businesses, compliance helps in identifying and mitigating risks related to financial, operational, and reputational matters, safeguarding against potential losses and liabilities. It is crucial for fintechs or any other financial entities to adopt the best compliance practices to avoid regulatory scrutiny.

Hence, Skydo has prioritised developing policies and processes to ensure individuals and businesses onboard Skydo do not have to worry about any lapses in compliance for cross-border transactions.

When you sign up with Skydo, it handles your personal information carefully, strictly following its extensive Privacy Policy. Access to your data is limited to authorised personnel, ensuring its security. If you want a smoother and more compliant payment platform, visit Skydo today.

Q1. Why is Paytm banned by the RBI?

Ans: The Reserve Bank of India banned Paytm Payments Bank because of unsatisfactory regulatory and supervisory compliance and for floating KYC and licensing norms.

Q2. Is Paytm payment bank being discontinued?