How to File Taxes Under 44ADA: GST for Freelancers

Being a freelancer is like running a one-person show – you're the writer, director, and star of your creative journey. But amidst the freedom and artistic endeavours, a villain sneaks onto the stage: tax filing. Imagine trying to decode complex tax forms while juggling creative projects – it's like performing a magic trick with too many hats.

As a freelancer, you must file ITR under ‘Income from business or profession’, where you can use Section 44ADA to simplify the process. However, you may need to register for GST.Tax management through compliance is as important when you have freelance income. Therefore, here is a detailed guide on filing taxes and adhering to GST regulations under Section 44ADA.

What is Section 44ADA of The Income Tax Act?

Under the section of presumptive taxation, taxpayers with Rs 2 crores as annual turnover or 3Cr if 95% of receipts are made through online payment modes are not required to maintain books of accounts, and the Income Tax Department presumes the profits to be 8% for cash receipts and 6% for digital credits.

Under Section 44ADA, the benefits apply to service providers such as freelancers. Now, freelancers or professionals such as lawyers, doctors, architects and others can declare their income at 50% of the annual gross receipts to limit their tax liability.

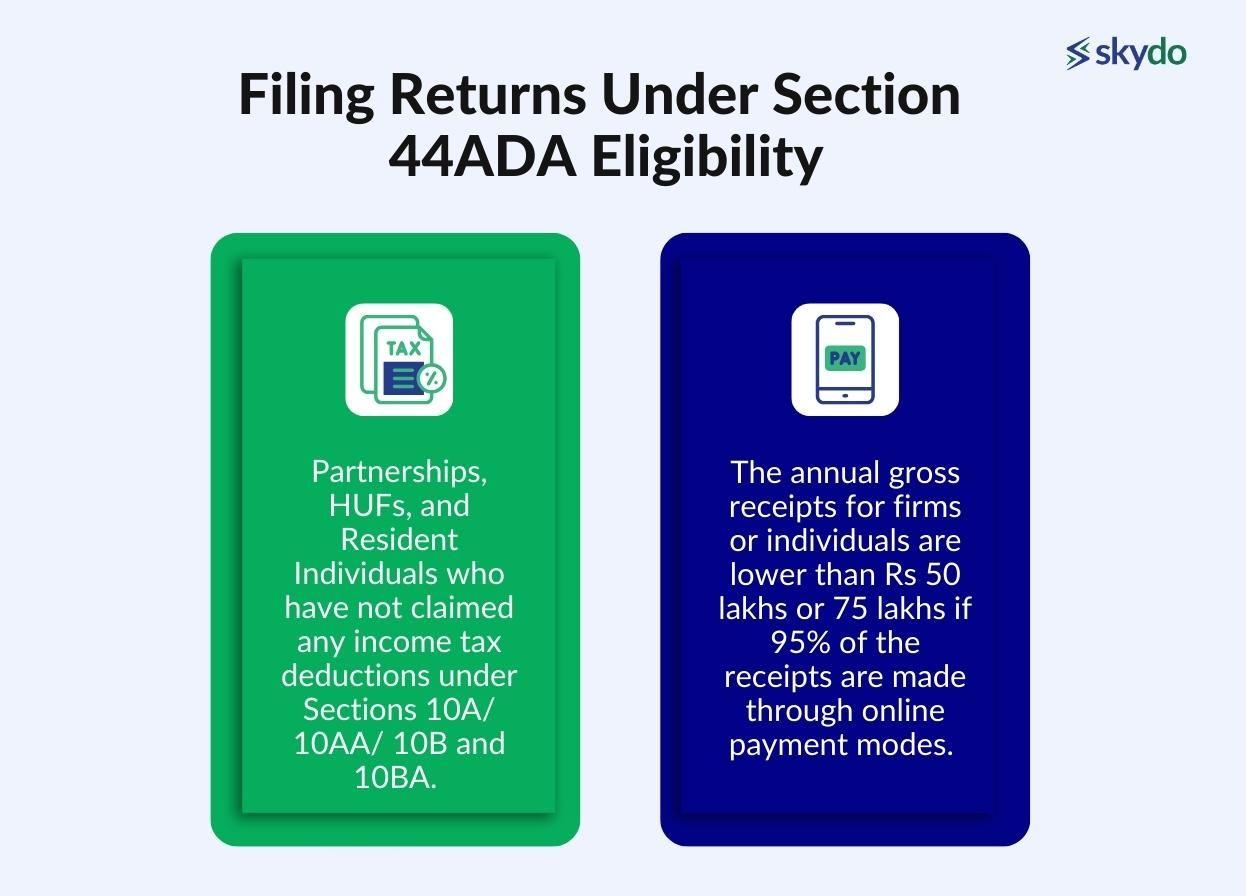

The following assessees are eligible to file returns under section 44ADA.

- Partnerships, HUFs, and Resident Individuals who have not claimed any income tax deductions under Sections 10A/ 10AA/ 10B and 10BA.

- The annual gross receipts for firms or individuals are lower than Rs 50 lakhs or 75 lakhs if 95% of the receipts are made through online payment modes.

Section 44ADA has allowed small taxpayers, especially freelancers, to ensure better tax management without maintaining the books of accounts and still comply with the relevant tax laws.

However, this section comes with some disadvantages, as an assessee choosing the section can not claim deductions under Sections 30 to 38 (including depreciation or unabsorbed depreciation). Furthermore, as per Sections 40, 40A, and 43B, no disallowances are permitted.

Budget 2023 Update for Sections 44ADA and 44AD

For the financial year 2023-2024 (assessment year 2024-2025), the Budget of 2023 has modified Section 44AD and Section 44ADA regarding presumptive taxation limits. The new limits are as follows.

| Sections | Previous limit | Updated Limt |

|---|---|---|

| 44ADA: For professionals like freelancers, sole proprietors, etc. | INR 50 lakh | INR 75 lakh |

| 44AD: For small businesses | INR 2 crore | INR 3 crore |

Calculate Presumptive Income under Section 44ADA of Income Tax

To opt for the Presumptive Taxation Scheme under Section 44ADA of the Income Tax Act, you must satisfy the following two criteria.

- The total revenue earned by the profession should not exceed INR 50 lakh

- The taxpayer must report at least 50% of the total revenue as income in the ITR

For instance, Dhruv is a freelance software developer. His total receipts for the financial year 2021-22 are Rs 40 lakh. His annual expenses are Rs 10 lakh towards rent, transportation, internet and mobile bills, travelling, etc.

Under normal provisions

Gross receipts - INR 40,00,000

Expenses - INR 10,00,000

Net profit will be Gross receipts - expenses, which is INR 30,00,000 (40,00,000 - 10,00,000)

Under the presumptive scheme

Gross receipts - INR 40,00,000

50% deemed expenses - INR 20,00,000

Net profit will be Gross receipts - deemed expenses, which is INR 20,00,000 (40,00,000 - 20,00,000)

In this case, Offering income under the presumptive scheme of taxation under section 44ADA is beneficial for Dhruv as the net profit is lower than the regular provisions.

How to File Taxes Under Section 44ADA

If you are a freelancer and have opted for the presumptive income scheme under Section 44ADA, you must file your taxes by filling up the ITR-4.

Here is the process to file taxes under Section 44ADA.

- Step 1: Register and log in to the ‘e-Filing’ portal of the Income Tax Department with a valid user ID and password.

- Step 2: Click on ‘e-file,’ ‘Income Tax Return,’ and ‘File Income Tax Return.’ Select the year and mode of filing (online) and click ‘Continue.’

- Step 3: Click on ‘Start New Filing,’ status as ‘Individual’ and click continue. Now select ‘ITR-4 from the drop-down menu and proceed.

- Step 4: Select the reason for filing the taxes and fill out all the required personal information such as name, PAN, address, Date of Birth, Aadhar number, email, mobile number, etc.

- Step 5: Fill out the required details in the ‘Gross Total Income’ section if you have any other income apart from freelancing and proceed.

- Step 6: Enter the presumption income under section 44ADA in the ‘Income for Business or Profession’ and choose the percentage of presumed profits (minimum of 50% of the gross receipts).

- Step 7: Specify the details about the disclosures and exempt income to provide details of financial particulars related to business, information regarding gross receipts reported for GST (Optional), and exempt income.

- Step 8: Add and verify any deductions you want to claim under Chapter VI-A of the Income Tax Act in the ‘Total Deductions’ section

- Step 9: Verify taxes paid by you in the previous year in the ‘Taxes Paid’ section for items such as TDS, TCS, Advance Tax, etc.

- Step 10: In the next section of ‘Total Tax Liability,’ you can view your computation of income, computation of tax, and total tax, cess, and interest. If there is a tax liability, you must click on ‘Pay Now’ or ‘Pay Later’ to make the tax payment.

If there is no liability and you are eligible for a tax refund, the website will lead you to the ‘Preview Return’ page.

- Step 11: After successful payment or submission, you will get a confirmation message displayed and be redirected to the ‘Back to Return Filing’ portal.

- Step 12: Preview your return and click ‘Proceed to Validation’. If there are some errors, they will be displayed, and you need to correct the errors and click on ‘Complete your Verification.’ You can e-verify your return to complete the mandatory process of return verification.

GST For Freelancers: An Overview

As an earning citizen, a freelancer must pay income tax on all the earnings during a financial year based on the applicable tax slabs. However, if your annual turnover exceeds Rs 20 lakhs in a financial year, you must register under GST.

The earnings include services rendered domestically and internationally with other incomes including commissions, fees for independent work, and reimbursements, also counting towards 20 lakhs.

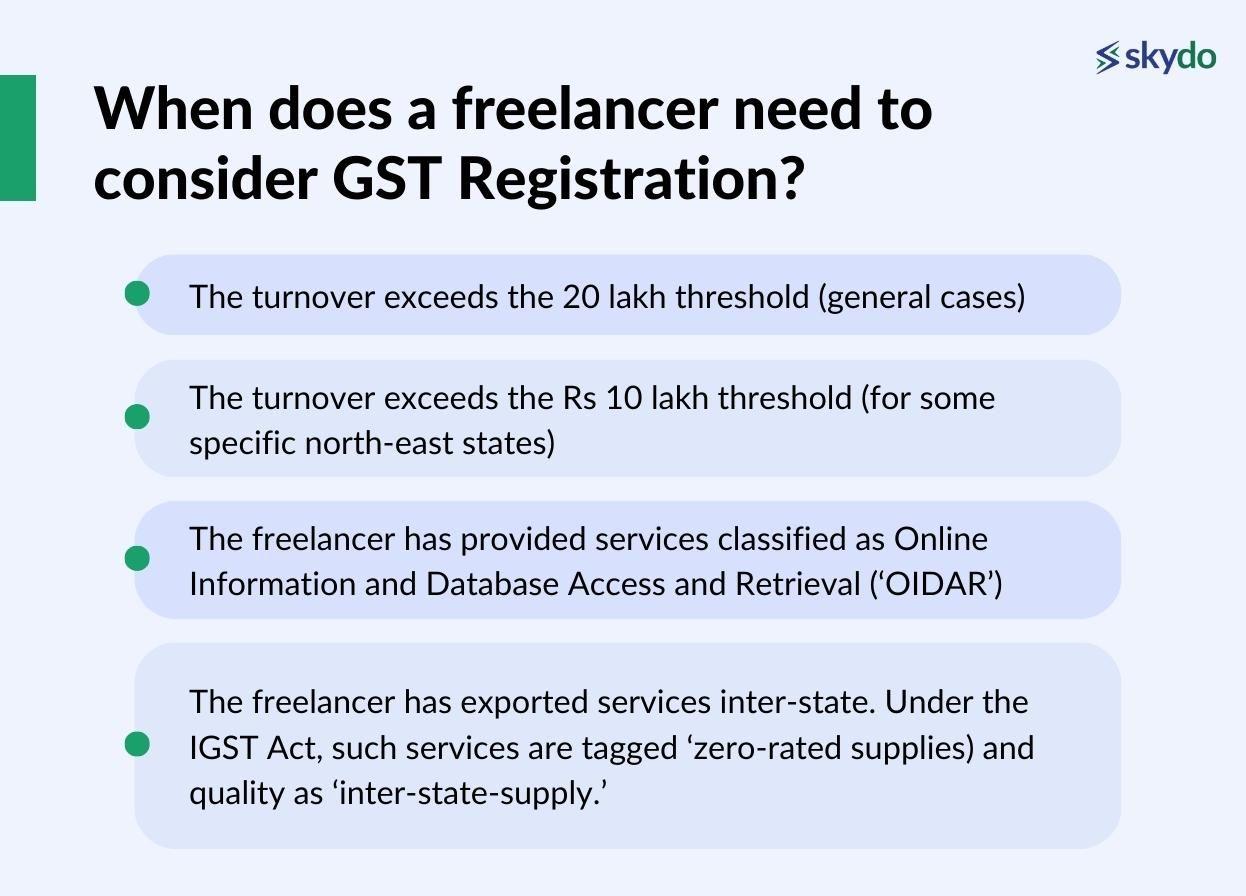

As a freelancer, you are required to register for GST when:

- The turnover exceeds the 20 lakh threshold (general cases)

- The turnover exceeds the Rs 10 lakh threshold (for some specific north-east states)

- The freelancer has provided services classified as Online Information and Database Access and Retrieval (‘OIDAR’)

- The freelancer has exported services inter-state. Under the IGST Act, such services are tagged ‘zero-rated supplies) and quality as ‘inter-state-supply.’

The Indian government has made it simpler for freelancers to register under GST and pay the applicable tax. You can choose between the following GST schemes If you are a freelancer.

- Composition Scheme

The Indian government launched the Composition Scheme in 2019 for small businesses with an annual turnover of less than Rs 1.5 crore. However, they extended the scheme to service providers such as freelancers.

Freelancers having an annual turnover of less than Rs 50 lakhs can opt for the scheme and have to pay 6% GST (3% CGST and 3% SGST).

- Regular Scheme

The Regular Scheme is the fundamental method for registering and paying GST for freelancers. If you do not opt for the composition scheme, you have to pay GST based on four different slabs: 5% GST, 12% GST, 18% GST, and 28% GST, depending on the nature of the category of services.

However, if there is no specific category of the services rendered by the freelancer, 18% GST is applicable.

Types of GST and their Filing Process

Although there are 22 types of GST returns, only 11 are active. For a freelancer, the following three types of GST are applicable.

GSTR-1

It is a return that a freelancer must furnish regarding the details of all the outward supplies of services. You must provide details by filing the GSTR-1 extend to all the invoices and debit-credit notes for the year. The filing frequency of GSTR-1 is as follows.

- Monthly by the 11th of every month: If the annual turnover exceeds Rs. 5 crores and the assessee has not opted for the QRMP scheme.

- Quarterly by the 13th of the month following every quarter: If the assessee has opted into the QRMP scheme.

GSTR-3B

It is a return to be filed by the freelancer every month as a self-declaration regarding the summarised details of all the outward services rendered, including tax liability, input tax credit claimed, and taxes paid. The filing frequency of GSTR-3B is as follows.

- Monthly by the 20th of the succeeding month: The annual turnover exceeds Rs 5 crores, but the assesses have opted out of the QRMP scheme.

- Quarterly by the 22nd of the month following the quarter for the ‘X’ category of states and the 24th for the ‘Y’ category of states: The annual turnover is equal to or below Rs 5 crores, and the assessee has opted into the QRMP scheme.

GSTR-9

The requirement to file GSTR-9 applies to all GST-registered entities except-

- Input service distributors

- Casual taxable persons

- Non-resident taxable persons

However, if you have an annual turnover of more than Rs. 2 crore, you must file a GSTR-9 or GST Annual Return.

It is the annual GST return to be filed by a freelancer by December 31 of the year following the applicable financial year. The return filed contains all the inward and outward services received or rendered during the year under different tax heads, such as CGST, SGST, and IGST.

Additionally, it also contains the value of services provided under every HSN code with details of taxes paid and payable. The GSTR-9 is a consolidated summary of all the monthly and quarterly returns (GSTR-1, GSTR-2, GSTR-3B) during that financial year.

Here is the process of filing GST returns.

- Step 1: Log in to the GST portal using your GSTIN number, click on ‘Services,’ and click on the ‘Returns Dashboard’ from the ‘Returns’ section. Fill in the financial year and the return filing period.

- Step 2: Select the return you want to file and click ‘Prepare Online.’ Enter all the required information and click on ‘Save.’ Click on the ‘Submit’ button after a success message is displayed.

- Step 3: Click on the ‘Payment of Tax’ button, ‘Check Balance,’ and next to ‘Clear Your Liabilities,’ mention the amount of credit you want to use for the available credit balance. Click on ‘Offset Liability’ and make the payment. Then click on ‘OK’.

- Step 4: Check the box for the declaration and select an authorised signatory from the drop-down menu. Click ‘File Form With DSC’ or ‘File Form With EVC’ and click ‘Proceed’. Make the payment to complete your GST filing.

Key Points to Remember

Here are some key points to remember while filing taxes or GST under Section 44ADA.

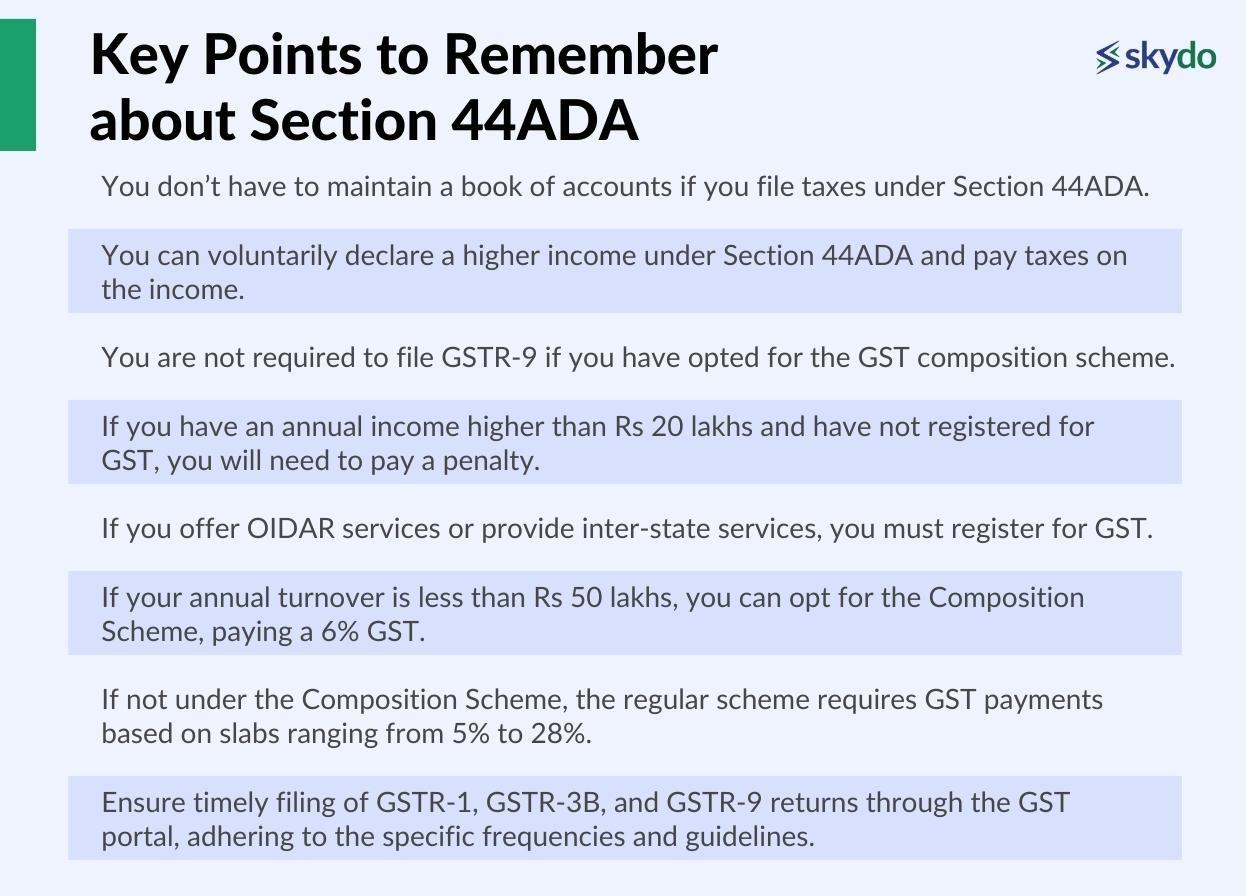

- You don’t have to maintain a book of accounts if you file taxes under Section 44ADA.

- You can voluntarily declare a higher income under Section 44ADA and pay taxes on the income.

- You are not required to file GSTR-9 if you have opted for the GST composition scheme.

- If you have an annual income higher than Rs 20 lakhs and have not registered for GST, you will need to pay a penalty.

- If you offer OIDAR services or provide inter-state services, you must register for GST.

- If your annual turnover is less than Rs 50 lakhs, you can opt for the Composition Scheme, paying a 6% GST.

- If not under the Composition Scheme, the regular scheme requires GST payments based on slabs ranging from 5% to 28%.

- Ensure timely filing of GSTR-1, GSTR-3B, and GSTR-9 returns through the GST portal, adhering to the specific frequencies and guidelines.

Expert Advice and Resources

Filing taxes and GST under Section 44ADA may seem complex. Here is some expert advice and resources you can use if you have freelance income.

- You must maintain a proper book of accounts if you have presumptive profits lower than 50% under Section 44ADA. You may need to perform an audit as well.

- There are numerous online GST calculators which you can use to calculate your applicable GST liability and file your GST effectively.

- You can visit the Income Tax Department’s website or the GST portal for regular updates on Section 44ADA and applicable GST regulations.

Conclusion

Similar to other income earners, freelancers must comply with the income tax and GST regulations based on their nature of services and the amount of annual turnover. Section 44ADA is a beneficial section that mitigates the efforts of maintaining extensive books of accounts through presumptive taxation, resulting in better tax management for individuals earning freelance income.

A similar is the case with filing GST, which ensures better compliance for freelancers earning more than Rs 20 lakhs annually.

FAQs on Section 44ADA

Q1. What is section 44ADA?

Ans: Section 44ADA of the Income Tax Act is a provision that allows certain professionals, including freelancers, to declare their income at 50% of their annual gross receipts for tax purposes.

This section simplifies tax compliance for small taxpayers, relieving them from the need to maintain detailed books of accounts. However, deductions under specific sections are not allowed under this scheme.

Q2. What is the difference between 44AD and 44ADA sections?

Ans: Section 44AD and Section 44ADA pertain to presumptive taxation schemes. However, they have different applicability and benefits.

Section 44AD is for businesses, while Section 44ADA is for professionals like freelancers. Section 44AD allows for presumptive income at 8% of turnover, while Section 44ADA allows professionals to declare income at 50% of annual gross receipts. The key distinction lies in the type of taxpayers each section caters to.

Q3. What is a Presumptive Taxation Scheme?

Ans: A Presumptive Taxation Scheme is a simplified tax regime that allows eligible taxpayers, such as small businesses and professionals, to declare their income at a prescribed percentage of their total turnover.

It eliminates the need for maintaining detailed accounts and records. Section 44AD and Section 44ADA are examples of such schemes under the Income Tax Act.

Q4. I am a freelancer, and I opted for Presumptive Scheme u/s 44ADA. Can I claim expenses like internet, rent, travelling, etc.?

Ans: Under Section 44ADA, you cannot claim deductions for expenses. Your income is presumed to be 50% of your annual gross receipts, and no deductions for expenses, including internet, rent, or travel, are permitted.

Q5. Is it necessary to pay advance tax if I choose the Presumptive Taxation Scheme under Section 44ADA?

Ans: If you opt for the Presumptive Taxation Scheme under Section 44ADA, you must pay advance tax if your estimated tax liability for the financial year exceeds Rs. 10,000. Advance tax is typically paid in monthly instalments to ensure timely tax payments.

Please note that these answers provide a brief overview of the questions posed. For detailed tax advice and specific queries, it is advisable to consult a tax professional or refer to official tax authorities.