Pros and Cons of Cross Border Payment Solutions

"The current state of cross-border payments is not fit for the 21st century."

Mr. Ravi Menon, the Managing Director of the Monetary Authority of Singapore, said this in his speech at the Annual SWIFT International Banking Operations Seminar, 2022.

The Indian Payments Handbook 2022-07 explains two prevalent challenges with cross border payment solutions –high transaction cost and the long duration for end-to-end settlement of cross-border payments. The average price of receiving inward remittance is 6% at present. The United Nations is working on reducing this cost to 3% by 2030. In fact, it is one of their Sustainable Development Goals (SDG).

Furthermore, according to the Handbook, India is the largest market for inward remittance flow, making seamless cross-border transactions crucial for the economy.

However, these challenges serve as the biggest threats to the business landscape. It means letting go of a significant sum in every transaction and delays in receiving payments. These factors trigger critical issues such as cash flow, reduced profit margin and increased debt.

Payment platforms, like Skydo, aim to revolutionise the sector by making cross-border payments more efficient and cost-effective. Let's understand the pros and cons of cross border payment solutions in detail and how to choose the right payment gateway.

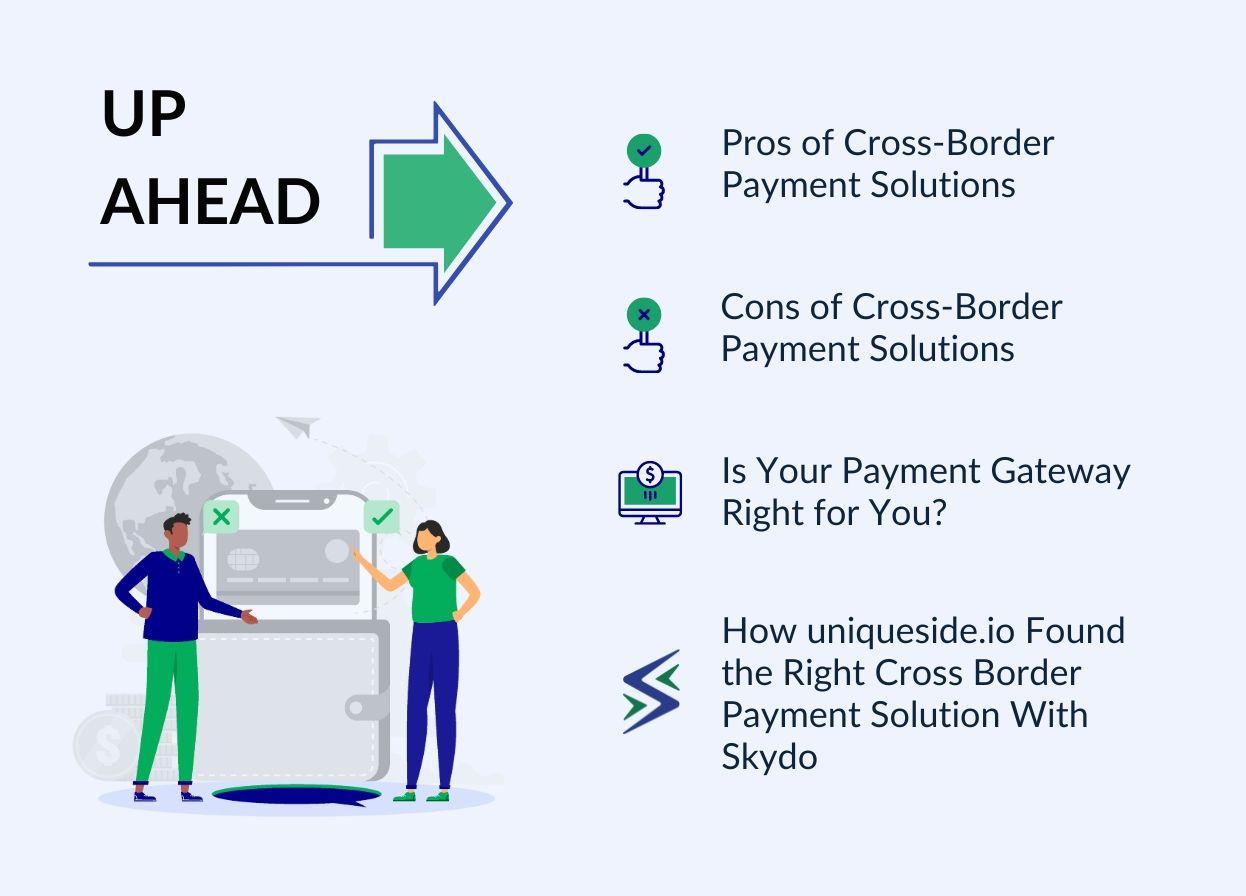

Pros of Cross-Border Payment Solutions

Currently, the most common ways to send money across borders are through banks, credit cards, e-money wallets, and mobile payments. These methods often depend on systems like SWIFT or the related payment platform. As a result, international transactions are usually slower, more expensive, and less transparent than domestic ones.

Hence, cross border payment solutions are fundamental for business growth and expansion. Here is how they help businesses receive global payments seamlessly by tackling regulatory challenges.

1. Global Reach and Expansion

Many businesses are sceptical of offering their services or products to international clients because of payment delays. However, cross border payment solutions like Skydo help receive cross-border payments quickly by incurring low costs.

This enables entrepreneurs to expand their business globally, get access to a large client base, and boost revenue.

2. Faster Transactions

Cross border payment solutions can accelerate transactions and optimise cash flow. The processing time for global payments through banks is around 5-10 days. However, it can take up to a month if the transaction gets stuck due to regulatory challenges or inadequate details.

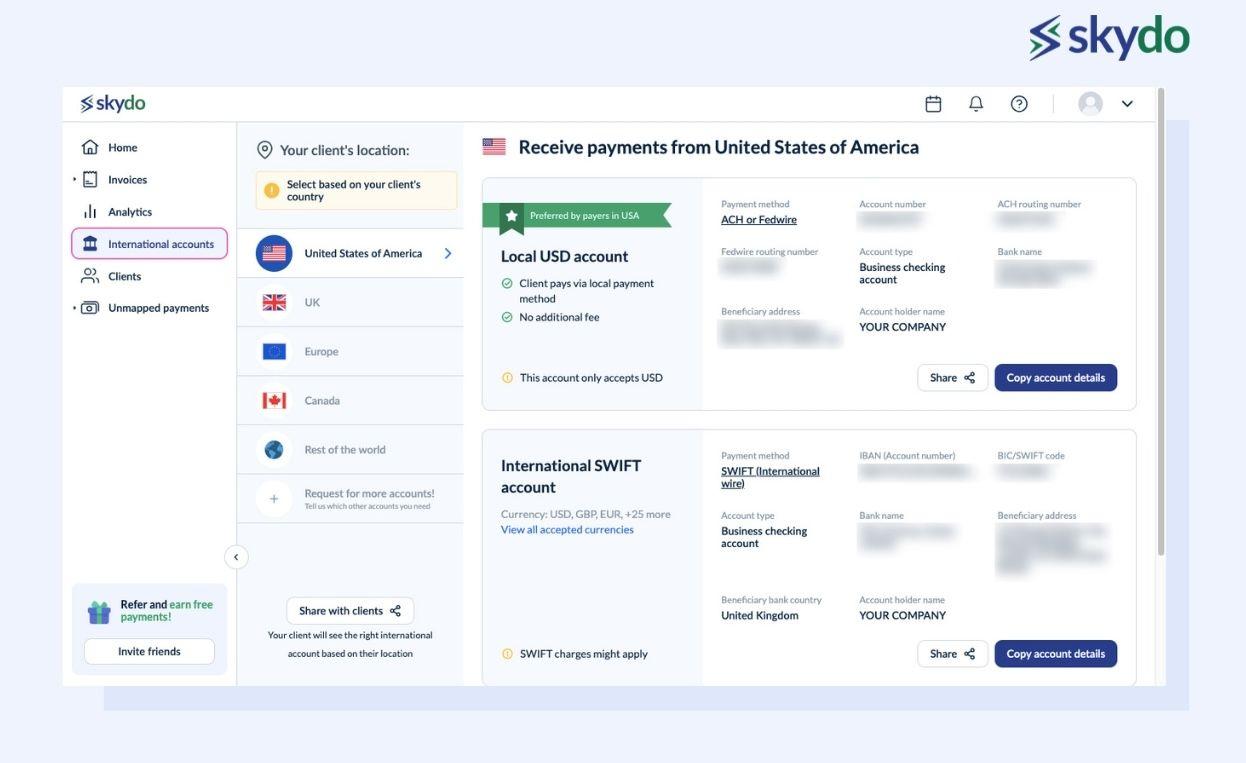

Digital payment gateways like Skydo significantly reduce the processing time for cross-border payments by opening a virtual bank account for your business in another country.

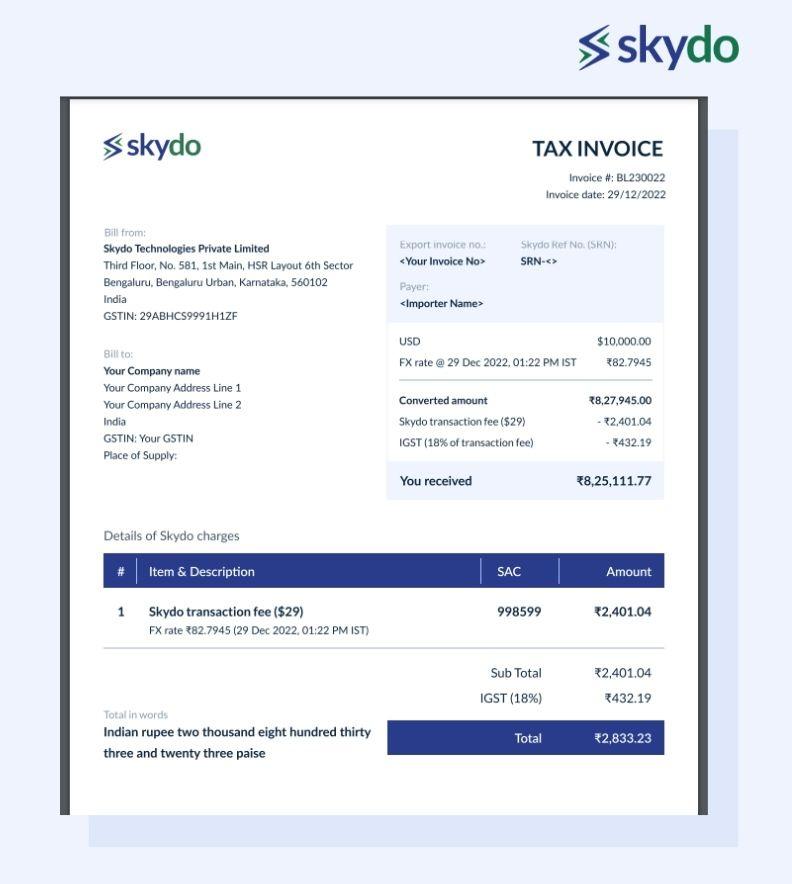

This way, the client can remit the money to your virtual bank account in the respective country, which will pass through the Skydo platform and into your bank account maximum within T+2 days. You can further track this whole journey through the tracker available against each invoice.

3. Currency Conversion and Risk Management

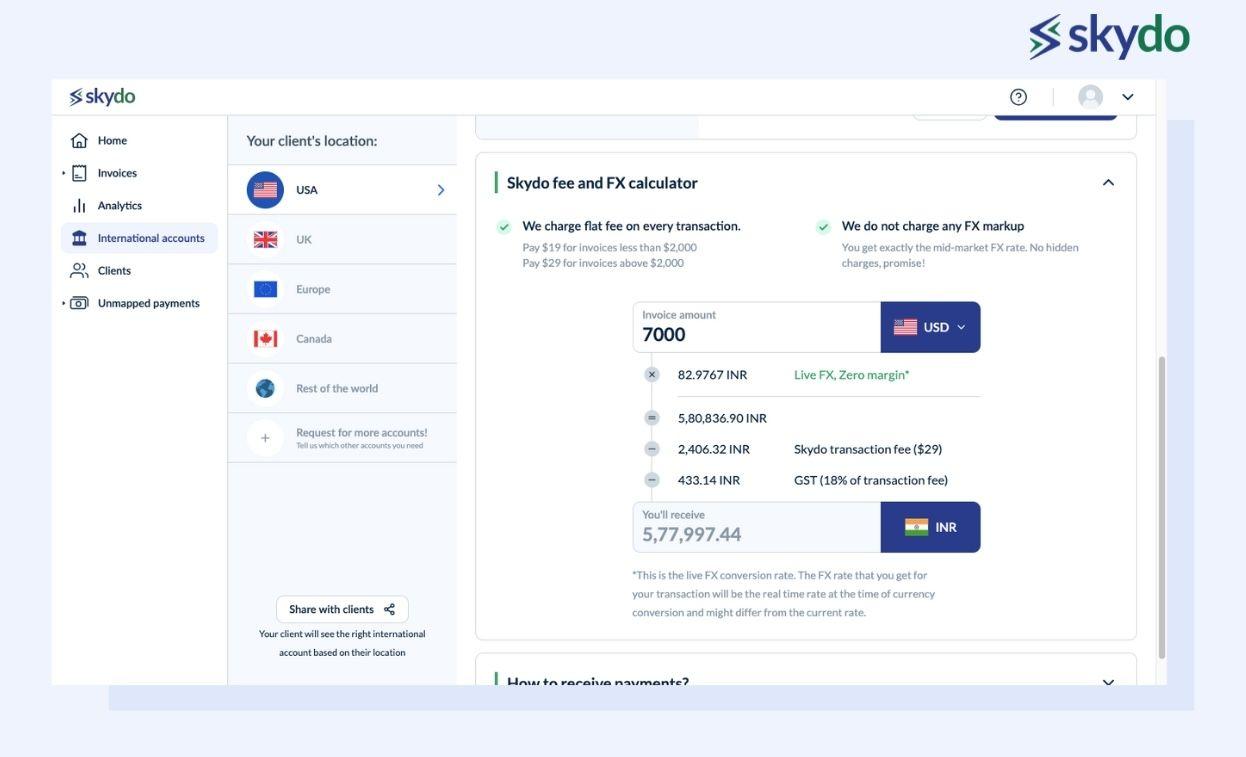

In tech service exports, businesses often lose money due to currency conversion fees and additional hidden charges. Skydo’s cross border payment solution offers transparent currency conversion by displaying real-time exchange rates.

They also offer competitive exchange rates and help businesses calculate the accurate currency cost compared to traditional banks.

Some payment gateways also help manage currency conversion risk by offering hedging options. It allows businesses to hold their payments securely in case the value of the foreign currency depreciates.

4. Enhanced Security and Fraud Prevention:

According to a survey, fraud in global payments is a concern for 56% of businesses. Moreover, 52% of them also consider data theft during payment transactions as one of the significant risks in international payments.

cross border payment solutions mitigate this risk by offering enhanced security measures. Payment gateways use artificial intelligence systems to detect and stop fraudulent activities.

Learn more: Breaking Barriers, Bridging Borders: How Skydo Increased Success Rate on International Payments

Cons of Cross Border Payment Solutions

While cross border payment solutions have been a game changer for businesses in expanding their services to international markets, there are four significant challenges - cost, speed, access and transparency.

1. Fees and Charges

High transaction cost is a significant roadblock to receiving global payments. The complexities arise primarily because a) multiple currencies are involved and b) various channels or levels in payment flow, such as banks, payment facilitators and payment operators exist.

The average cost of international wire transfers is between $15-$75 per transaction. Therefore, before you choose a payment gateway, research and compare the transaction value in-depth, currency conversion, and processing fees charged by cross border payment solutions. Moreover, you must be aware of any hidden costs levied by the payment service provider.

2. Regulatory and Compliance Challenges

Regulatory challenges and adherence to international financial compliances are massive obstacles while dealing with cross border payment solutions. Businesses have to navigate through anti-money laundering laws in foreign countries. Global payments often get stuck in regulatory processes, leading to unnecessary delays.

3. Exchange Rate Fluctuations:

Studies suggest that foreign exchange rate volatility harms cross-border imports and exports. Multiple currencies are involved, and the value can change at the time of the payment. If the value of the foreign currency decreases, your earnings in Indian currency might take a direct hit.

The best way to avoid exchange rate risk and receive accurate payments is to quote proposals in INR.

Learn more: How Much Forex Fees Do You Pay on Your International Transactions

4. Lack of Remittance Information:

"The biggest issue is when I receive a wire: What does it relate to? What invoice specifically or a combination of invoices does it relate to?” — A large company in Chicago during the B2B Wire Transfer Payments Study commented.

Receiving global payments through wire transfer does not provide much remittance information, making it difficult to reconcile payments with invoices, especially if multiple invoices are sent to a single client.

According to a study, 94% of people consider remittance information valuable. However, cross border payment solutions often fail to provide this information, leading to extra manual efforts.

5. Customer Experience

A seamless customer experience is the backbone of an efficient global payment system. However, business owners and account managers are forced to spend time choosing the suitable currency, dealing with currency exchange rates and resolving language barriers on cross-border payment platforms.

Moreover, businesses often have to worry about data security, facing regulatory challenges, payment delays and hidden charges, making the whole process cumbersome.

Learn more: Don’t Stay in the Dark Anymore: Monitor Your International Payments From Sender Account to Your Account

6. Technical Glitches and Downtime

Another issue with cross border payment solutions is the disruption of digital payments through technical glitches, downtime, or software failures. This can lead to delays or failure in receiving global payments. It further results in loss of revenue, extra transaction charges, operational inefficiencies, and customer dissatisfaction.

However, you can mitigate the risk caused by downtime by creating a contingency fund that they can use in emergencies. You must also recommend negotiating the payment terms with the customers and vendors to receive advance payments.

Is Your Payment Gateway Right for You?

The world is witnessing an embedded finance revolution where individual consumers and businesses are not relying solely on banks for their financing needs. Finding the most suitable payment gateway becomes more stressful. Here is a quick and simple guide to help you shortlist the ideal cross border payment solutions for your business.

1. Assessing Your Business Needs

When onboarding vendors, it's crucial to assess if they can effectively address your unique business challenges and contribute to your growth.

You can understand payment gateways like a business vendor or a partner. However, before collaborating with them, you should evaluate your business requirements, such as the frequency, volume and nature of payment transactions, and your business goals.

You should also consider or explore payment gateways to assess various aspects like credit card acceptance, online checkout experience, transaction volume, security, international transactions, returns, and integration with your e-commerce platform.

A seamless returns and refunds process through the payment gateway can enhance customer satisfaction.

Assess the payment gateway's integration with your e-commerce platform to ensure smooth data flow between systems.

Evaluate the reporting and analytics features provided by the payment gateway for informed business decision-making.

Consider the quality of customer support offered by the payment gateway as it can be crucial in resolving issues promptly.

Understand the fee structure associated with the payment gateway, including setup and transaction fees, to align it with your budget.

Ensure the payment gateway can accommodate your business's future growth without significant disruptions.

2. Researching Payment Gateway Options

Once you assess your business needs, you must choose the right payment gateway whose features align with your business requirements.

One of the best ways to do this is to conduct comprehensive market research, shortlist popular payment gateway providers, and consider the pros and cons and the features offered by the service providers.

To ensure that cross border payment solutions offer a frictionless payment journey, you can consider factors like transaction fees, quick customer support, and simple integration into your existing accounting system.

3. Seeking Professional Advice

A key feature of embedded finance is that non-financial customers get easy access to financial products and technologies. It may, however, serve as a drawback for business owners who are unaware of fintech products or technologies.

Hence, before you integrate cross border payment solutions, you can consult business advisors or financial experts to find the ideal payment gateway for your business. They can assess your business needs, do risk assessment, and cost analysis, and ensure that the platform solves the regulatory challenges.

How Uniqueside.io found the right cross-border payment solution with Skydo

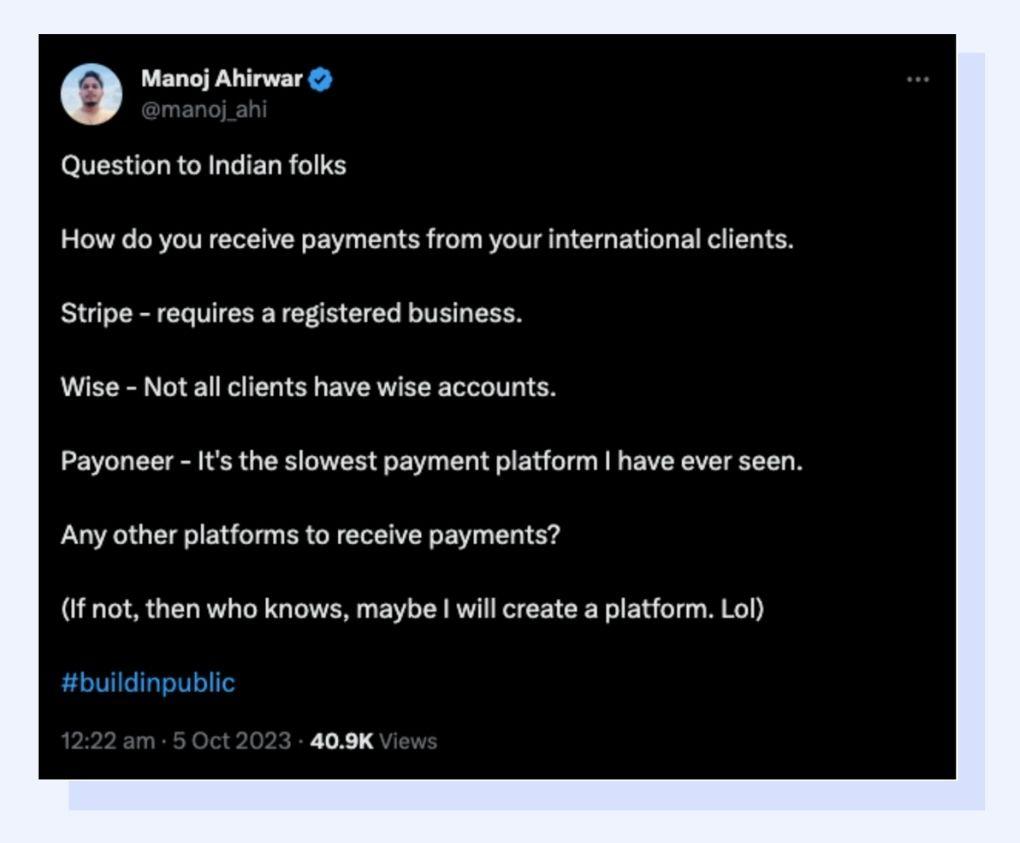

In July 2023, Manoj Ahirwar, Founder, Uniqueside.io embarked on a new journey as he left his job in Singapore to start his software development company, Uniqueside. The dream was taking shape, but a significant hurdle awaited me in the realm of payment platforms.

His first client payment through PayPal was cut down by hefty fees, leaving him with just $2,850 out of a $3,000 payment. This substantial loss prompted him to search for a more cost-effective and efficient solution to accept payments from the United States.

This quest led me to Wise, a platform promising lower fees. However, while Wise's user interface was impressive, its data functionality left much to be desired. Moreover, obtaining the Foreign Inward Remittance Certificate (FIRC) proved complex and time-consuming.

In September, he acquired another client, and his troubles with Wise escalated. Attempting to set up a Wise account for the new client led to a frustrating 10-day project delay. He took to Twitter to share his woes, hoping to find a better solution.

His tweet caught the attention of the Google algorithm, which began suggesting alternative payment platforms. It was through this recommendation that he stumbled upon Skydo.

"Skydo has been a game-changer for my software development company, Uniqueside. After struggling with exorbitant fees and inefficiencies on other payment platforms, I stumbled upon Skydo, and it was a breath of fresh air. The onboarding process was smooth, the user interface was top-notch, and the team was receptive to user feedback.

Skydo has saved me money and valuable time, allowing me to provide better service to my clients. It has become my primary payment platform, and I couldn't be happier with the decision. Skydo has become an invaluable partner in the success of Uniqueside."

Conclusion

Currency exchange fluctuations, conversion fees, and complex regulatory challenges create potential delays, making cross-border payments nothing less than a nightmare for businesses.

Cross-border payment solutions enable businesses to expand their business globally. However, despite the various benefits, they also pose significant challenges for businesses, making it difficult to manage their core business activities. Hence, choosing the right payment gateway not only improves efficiency but also helps you save on extra costs.

One-stop cross-border payment solutions like Skydo streamline global payments and rescue businesses from getting entangled in the web of regulatory challenges.

Request a demo with Skydo to receive cross-border payments seamlessly and unlock global opportunities for your business!