Everything You Need to Know About Embedded Payments

There has been notable growth in the payments industry in the last ten years, driven by technological advancements and user experience improvements.

The emergence of a new cohort of payment processors, payment methods, value-added services, and infrastructure providers has further accelerated this progress. These innovations respond to the increasing customer demand for more straightforward payment procedures, especially online payments.

This blog will shed light on embedded payments and how they are helping businesses streamline their payment processes.

What Are Embedded Payments?

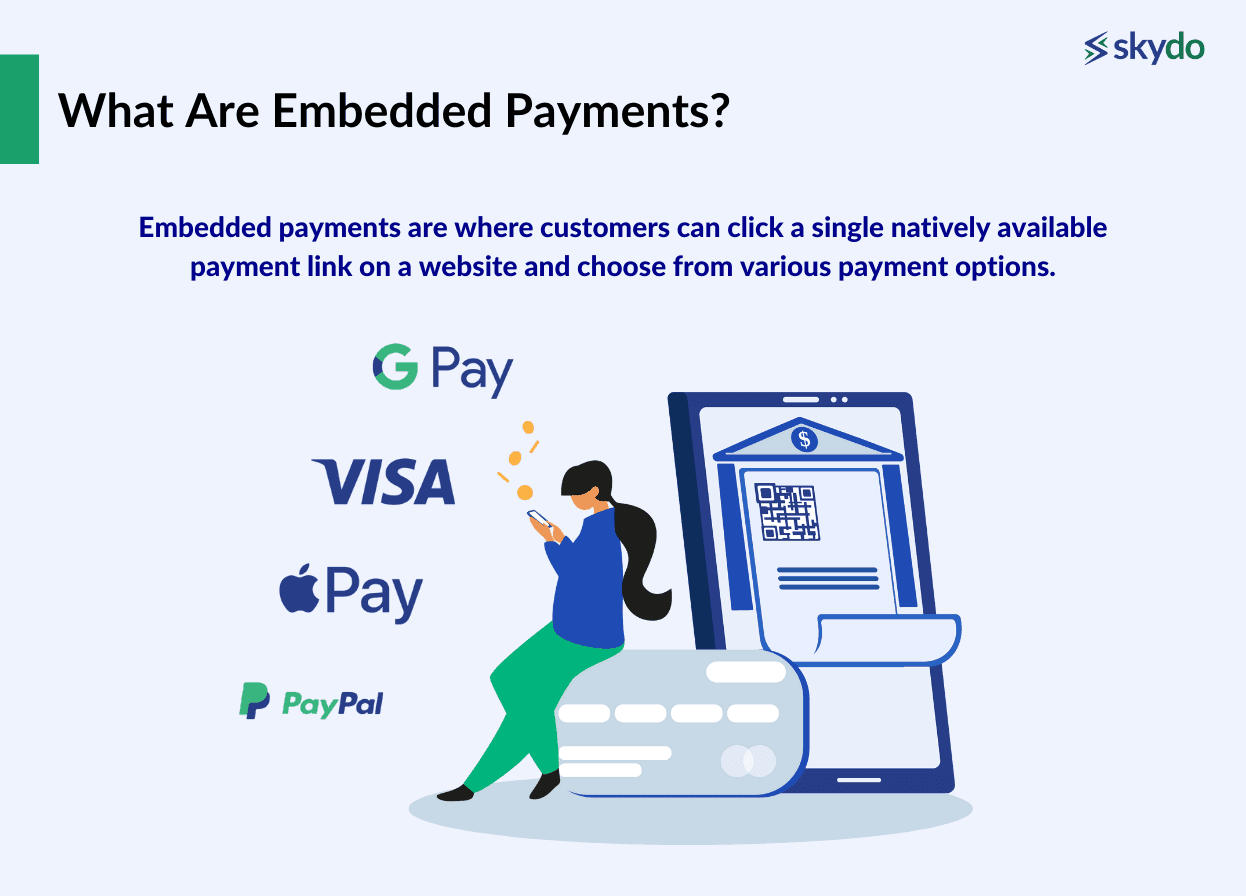

Embedded payments are where customers can click a single natively available payment link on a website and choose from various payment options. They allow companies to ensure customers do not have to leave their websites or mobile applications to pay for a product or service.

For example, if you are buying a product from Amazon, embedded payments allow you to make online payments for the product without having to leave the website or the app. Furthermore, you can choose from multiple payment methods at your convenience.

Most embedded payments fall under the umbrella of embedded finance. Embedded finance definition refers to a process, where third-party payment providers such as banks and financial institutions offer their services to execute single-click payments. In most cases, embedded payments are executed with pre-saved payment credentials on the websites or the apps.

Embedded payments differ from traditional checkout processes, as in traditional checkouts, users are redirected to a separate payment page hosted by a third-party payment provider. This page may have a different look and feel from the rest of the website, which may be a less smooth and cohesive user experience.

How do Embedded Payments Work?

Embedded payments are made possible and successful because third-party providers developing API tools. These API tools allow these third-party payment providers to integrate their payment systems on other websites and mobile applications.

For tech-enabled platforms and mobile applications, embedded payments work using two methods–natively or through utilising a third-party provider.

1. Registered Payment Facilitator (PayFac)

The PayFac model is used by big companies such as Shopify, Uber, Stripe, etc. The payment provider encourages companies to facilitate transactions on their behalf directly from the websites or mobile apps. The companies integrate a processor or payment gateway into their platforms for seamless transactions.

The processor or the payment gateway works as an information intermediary between the platform and the customer’s bank and completes payments by securely transferring financial information. In such a case, customers can also save their payment credentials for the future to avoid entering the details every time and make faster payments.

A perfect example of the PayFac model is Uber, where you can book cabs and make immediate payments without leaving the app. Here, Uber works as a registered payment provider, permitted by available embedded finance providers to execute payments on their behalf.

2. Payfac-as-a-Service Model

Companies that aren’t substantially funded or have high resources look towards payfac-as-a-service. It provides all the advantages of embedded payments but in a cost-efficient way, that is simpler to execute and integrate.

The model requires companies who want embedded links on their platforms to work with third-party payment providers who facilitate embedded payments for businesses without requiring them to build the payment system natively.

A perfect example of payfac-as-a-service Paytm, registered with numerous banks and financial institutions but extends its services to other businesses to use its PayFac model to complete payments.

3. Full-Service Partnership

A full-service partnership is one of the most effective embedded payment models as it allows ISVs (independent software vendors), developers, and their customers to have a robust payment solution.

The partnership involves tightly integrating payment processing functionalities, and the platform providing the service takes care of all the included factors, such as pre-sales demos, pricing, marketing, onboarding, setup, and customer support.

Advantages of Embedded Payments

1. Increased Revenue

Embedded payments eliminate the need for users to navigate to external payment gateways, streamlining the purchasing process and reducing the likelihood of abandoned carts. They also facilitate subscription and recurring billing models, enabling businesses to establish predictable revenue streams and enhance customer retention.

Integrated payment systems allow for strategic placement of upselling and cross-selling prompts during checkout, boosting opportunities to increase the average transaction value. All these factors allow for increased revenue by reducing friction in the purchasing process.

2. Operational Efficiency

Embedded payments can automate tasks such as invoicing, reconciliation, and financial reporting, reducing the administrative burden on businesses. The effective integration provides real-time insights into transaction trends, customer behaviour, and other relevant metrics.

Embedded payments can help businesses comply with industry regulations and standards, such as the PCI DSS (Payment Card Industry Data Security Standard), by providing secure and compliant payment processing.

Embedded payments eliminate the need for users to input payment details repeatedly, offering convenience and speed. They come with robust security measures, instilling trust among customers. Furthermore, a smooth payment and user experience contributes to customer loyalty.

3. Additional Advantages

Embedded payments can facilitate entry into new markets by accommodating diverse payment methods preferred by customers in different regions. Businesses can innovate and optimise their strategies based on customer behaviour, preferences, and market trends as they can access payment data.

Implementing embedded payments positions businesses for the future, as it allows for flexibility in adapting to evolving payment technologies and consumer expectations

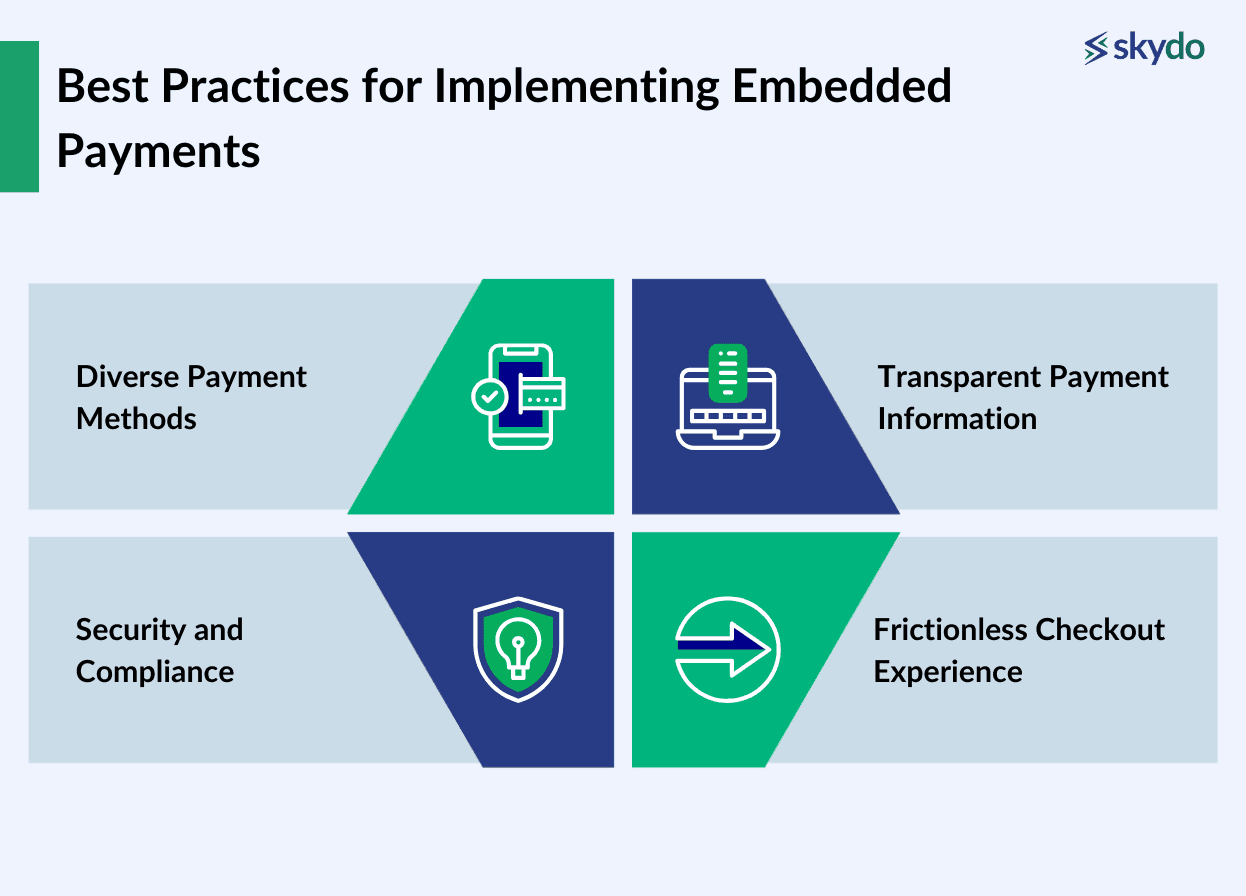

Best Practices for Implementing Embedded Payments

1. Diverse Payment Methods

Provide various secure payment options, including credit/debit cards, digital wallets (e.g., PayPal, Apple Pay, Google Pay, UPI interface), and alternative payment methods. Ensure that all payment methods adhere to industry security standards and are highly secure.

2. Security and Compliance

Stay informed about and comply with relevant regulations, such as the Payment Card Industry Data Security Standard (PCI DSS). Furthermore, regularly audit and assess security measures to address any vulnerabilities.

3. Transparent Payment Information

Communicate pricing details, including transaction fees, before checkout. Avoid hidden or unnecessary charges to build trust and transparency. Clearly define the terms and conditions that may affect the payment terms, such as GST, refund policy, etc.

4. Frictionless Checkout Experience

Create a simple and intuitive user interface for the checkout process. Minimise the number of steps required for a transaction to reduce user friction. Implement auto-fill features for forms and "Remember Me" options for returning users to reduce the effort required for repeat transactions.

Conclusion

The advent of embedded payments has revolutionised the way businesses engage with their customers and conduct transactions. Integrating seamless and secure payment functionalities directly into platforms and applications provides convenience and efficiency and enhances user experiences.

By offering a diverse array of secure payment options, ensuring rigorous user data security, complying with relevant regulations and providing transparent payment information, businesses can build trust and credibility in the minds of their customers.

However, you must analyse and compare the different embedded payment models to ensure you choose the most suitable one for your business. In case of confusion, consulting an expert is the best solution. FAQs

Q1. What are the risks of using embedded payments?

Ans: Embedded payments come with certain risks, such as data security concerns, inadequate regulatory compliance, integration challenges, dependency on third-party infrastructure, and transaction errors.

Q2. How much do embedded payments cost?

Ans: Embedded payments do not come with a cost for customers, but businesses have to pay a specific cost to the embedded payment provider. The costs range between 0.50% to 2% per transaction.

Q3. Do I need to be a financial expert to implement embedded payments?

Ans: While having a background in finance or expertise in financial matters can be beneficial, it's not a requirement to implement embedded payments. You can employ technical experts or take a full-service partnership to implement them.

Q4. What kind of platforms are suited for embedded payments?

Ans: You can implement embedded payments across platforms like e-commerce, mobile apps, subscription platforms, digital wallets, booking platforms, SaaS platforms, etc.

Q5. How can I get started with embedded payments?

Ans: You can start with embedded payments by understanding all three payment models and choosing the most suitable one. Thereafter, you can contact the service providers and create a business synergy. Integrating the required software in your platform is important to ensure successful embedded payment integration.