NOSTRO Account: What it is and How it Works for International Transactions

‘Good Things Take Time,’ and for hypothetical situations, this may give you hope and keep you going. But what about real-life situations? Is it good that you stand at the corner of the shop waiting for your online payment to succeed? Do you always have time to stand and look at the ‘Processing’ box, taking minutes while you think about the limited cash you have with you?

Now, imagine the same when you execute foreign currency transactions with the receiver in a foreign country, expecting you to pay immediately. A slow transaction processing speed can present you or your business in an unprofessional light and result in losing suppliers or vendors.

Almost every bank in India has different processing speeds for international transactions. The following factors explain the reasons behind fluctuating transaction speeds.

Factors affecting the processing speed of Foreign Currency Account Transactions

Every bank in India processes foreign currencies at different speeds as they rely on complex systems and operations to manage transactions, customer interactions, and regulatory compliance. Some key factors that can impact the processing speed of banks include the following.

1. Technological Infrastructure

The technology infrastructure of a bank, including its hardware, software, and network capabilities, plays a critical role in processing speed. Modern, well-maintained systems are more likely to handle transactions quickly and efficiently.

2. Correspondent bank relationships

Correspondent banks have extensive networks and relationships with other banks worldwide. They can route payments through the most efficient and cost-effective channels, reducing delays and transaction costs. However, with such extensive interconnected transactional systems, it is a hassle for a bank to execute transactions quickly.

While this network is designed to optimise the routing of international payments, it can also introduce some complexity. Each bank involved in the transaction needs to verify and process the payment. The more intermediaries involved, the more potential points of friction or delay in the process.

For example, an Indian business seeks to make an international payment of USD 10,000 to a U.S. supplier. To do this, the Indian business bank (Bank A) must use the services of correspondent banks in the U.S. due to its lack of a direct presence there. The payment travels through three banks: Bank A, Correspondent Bank X, and Correspondent Bank Y. Each bank conducts checks and verifications, potentially leading to delays and increased costs.

Additionally, international transactions can span different time zones and require communication between banks in various regions worldwide. This can lead to time lags as banks coordinate and confirm the transfer of funds. Delays may occur due to differences in working hours, holidays, or operational procedures across different countries.

The better the link between the two banks, the faster the processing time.

3. Compliance and regulatory adherence

Since foreign currency transactions fall under FEMA, correspondent banks must assist respondent banks in navigating the complex regulatory landscape of cross-border transactions. If the correspondent bank is well-versed in international banking regulations and compliance requirements, the processing time often takes less time.

4. Geographic reach and presence

Geographic reach significantly impacts the speed of foreign currency processing in international banking. Variations in time zones, specific payment timings, and using batch processing introduce delays. Banks operate within their local time zones, which can lead to misaligned working hours.

Batch payments, weekends, and holidays can further affect processing times. Banks with a global presence have an advantage, but real-time or emergency payments may come at a higher cost.

Notably, a specific category of banks can process these payments, known as AD-1 banks.

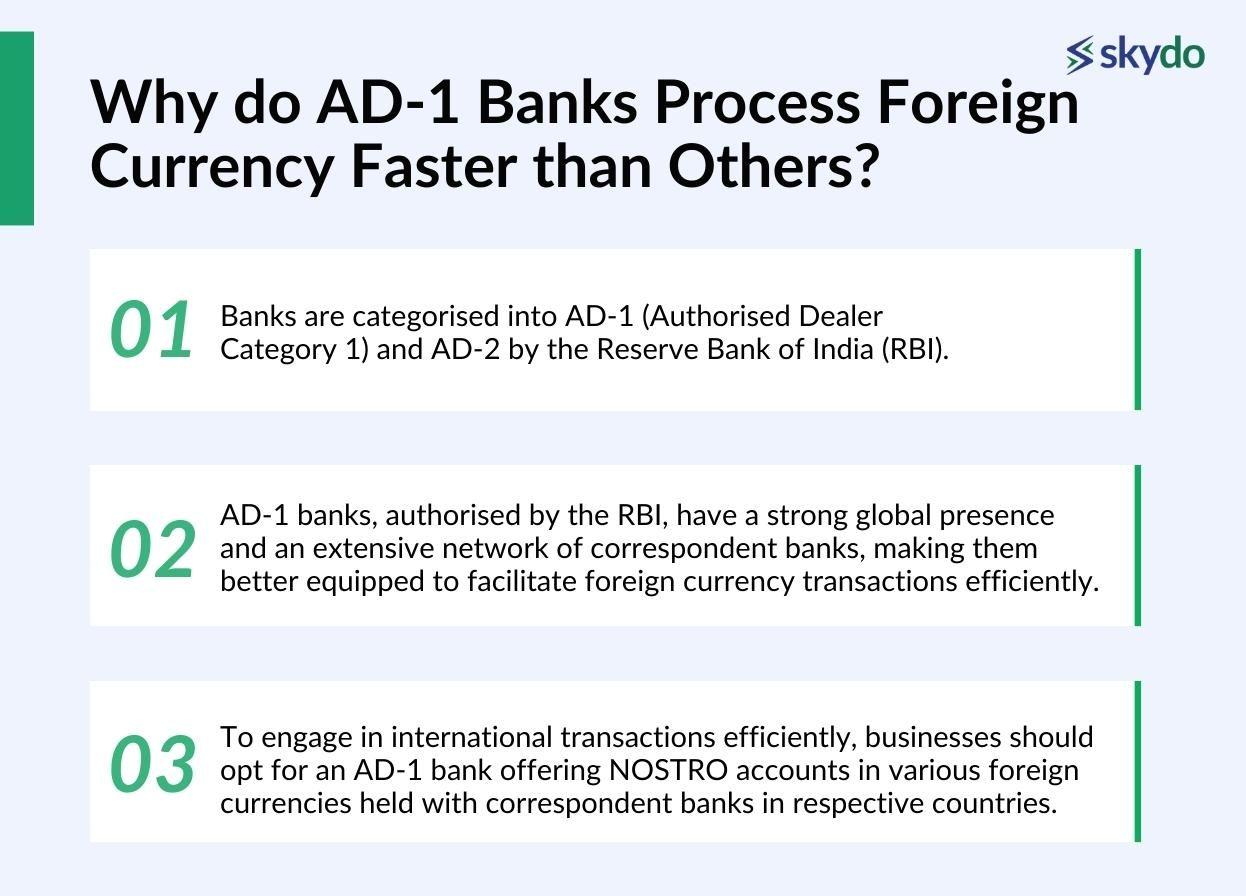

What are AD-1 Banks and Why do AD-1 Banks Process Foreign Currency Faster than Others?

Banks are categorised into AD-1 (Authorised Dealer Category 1) and AD-2 by the Reserve Bank of India (RBI). AD-1 banks are a significant presence in the international financial market and are authorised by the RBI to deal in foreign exchange transactions. These banks have a more extensive network of correspondent banks and are better equipped to facilitate foreign currency transactions more efficiently.

AD-1 banks provide a NOSTRO account service denominated in various foreign currencies. These accounts are held with correspondent banks or financial institutions in the respective foreign countries where the currencies are used. Therefore, for your business, you must choose an AD-1 category bank that provides a NOSTRO account service.

What is a NOSTRO account?

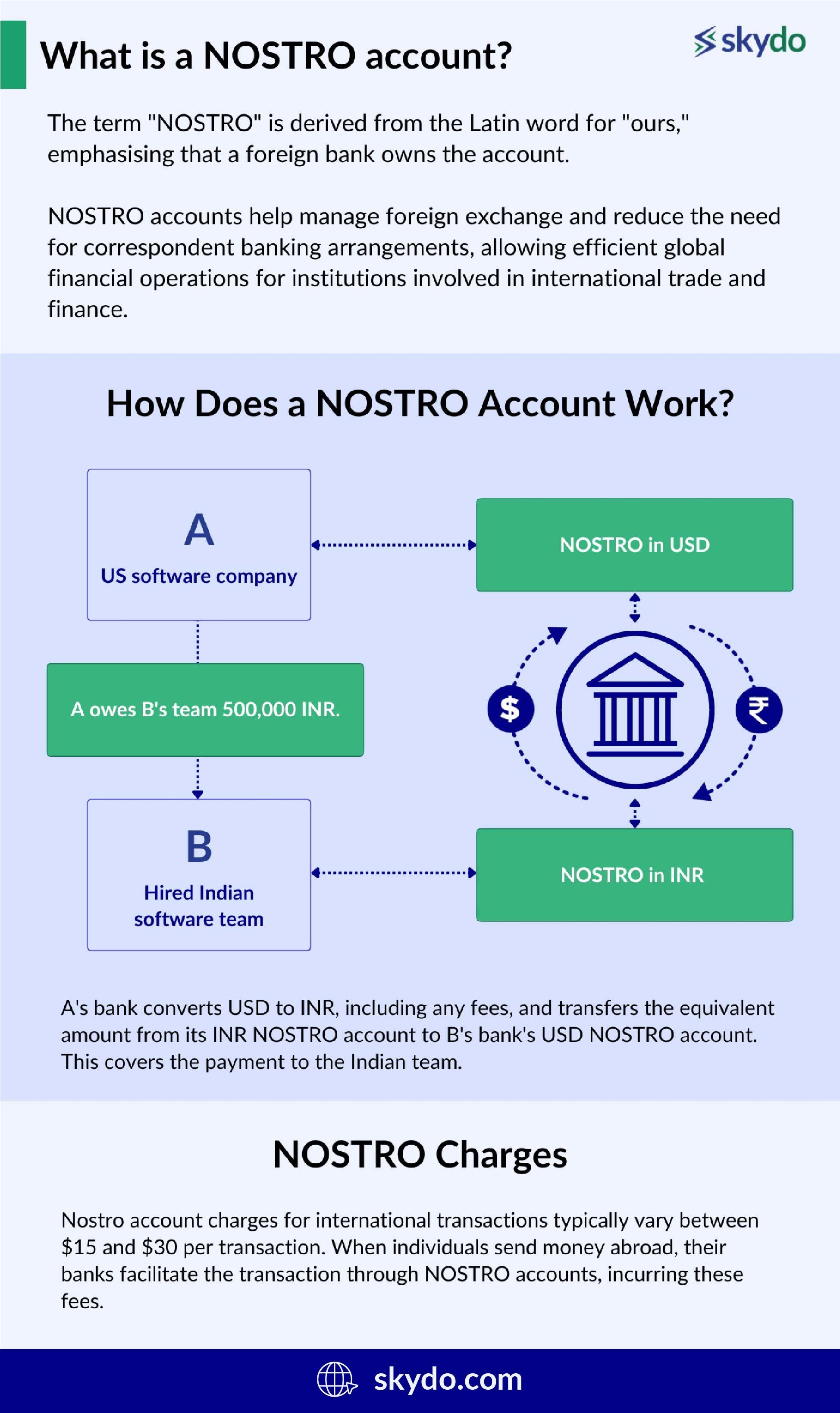

A NOSTRO account refers to an account held by a bank in a foreign country, denominated in the currency of that particular country. The term "NOSTRO" is derived from the Latin word for "ours," emphasising that a foreign bank owns the account.

These accounts facilitate international trade and transactions by enabling banks to hold funds in various currencies, simplifying cross-border payments and settlements. NOSTRO accounts help manage foreign exchange and reduce the need for correspondent banking arrangements, fostering efficient global financial operations for institutions engaged in international trade and finance.

How Does a NOSTRO Account Work?

NOSTRO accounts hold foreign currency at another bank in the respective country.

Here's a NOSTRO Account example to help illustrate how it works.

Let's consider US Company (A) and Indian Team (B).

- A US software company (A) hired your Indian software team (B).

- They need to pay you in Indian Rupees (INR), but the client mainly operates in US Dollars (USD).

- Both the US company's bank (A's bank) and your Indian team's bank (B's bank) set up special accounts called NOSTRO accounts.

- A's bank has a NOSTRO account in India for holding INR.

- B's bank has a NOSTRO account in the US for holding USD.

- A owes B's team 500,000 INR.

- A's bank converts USD to INR, including any fees, and transfers the equivalent amount from its INR NOSTRO account to B's bank's USD NOSTRO account. This covers the payment to the Indian team.

This way, NOSTRO accounts enable banks to facilitate cross-border transactions by maintaining balances in various currencies in foreign banks. These accounts act as liquidity buffers, ensuring the bank has sufficient funds in foreign currencies to process international payments and settle obligations.Most NOSTRO accounts are integrated with the SWIFT (Society for Worldwide Interbank Financial Telecommunication) messaging system. It sends payment instructions through SWIFT messages to its correspondent bank, which holds the NOSTRO account in the beneficiary's currency.

The correspondent bank can then execute the payment using the funds in the NOSTRO account. This process enables real-time or near-real-time settlement of cross-border transactions. NOSTRO accounts are also called VOSTRO accounts from the point of view of the foreign bank (Bank B).

What is a VOSTRO Account? & VOSTRO Account Example

A Vostro account is a financial arrangement where a domestic bank holds a bank account on behalf of a foreign bank or financial institution, denominated in the local currency of that country. Functioning as a form of correspondent banking, Vostro accounts facilitate foreign banks in executing transactions and delivering services in markets where they lack a direct presence.

Bank of America, based in the USA, aims to conduct business in India. To achieve this, they need to maintain an account with an Indian bank. Bank of America collaborates with ICICI Bank in India and opens an account with Indian Rupees (INR) as the currency. This account is called a VOSTRO account, and ICICI Bank is the domestic bank that holds it on behalf of Bank of America.

In this case, ICICI Bank provides various services to Bank of America, such as processing transactions, providing credit facilities, and managing the account. As a foreign bank, Bank of America can conduct business in India without having a physical presence there because of the VOSTRO account held by ICICI Bank.

NOSTRO Charges

NOSTRO accounts also play a pivotal role in the currency exchange process or currency conversion. If a bank needs to convert one currency into another to complete a cross-border payment, it can do so through its NOSTRO accounts.

For example, if Bank A in India wants to send Euros to a beneficiary in Europe, it can request the bank to use its NOSTRO account with a European bank to convert INR into euros for making the payment.

Nostro account charges for international transactions typically vary between $15 and $30 per transaction. When individuals send money abroad, their banks facilitate the transaction through NOSTRO accounts, incurring these fees. These charges contribute to the cost of conducting cross-border financial activities, reflecting the complexity of international transactions.

Difference Between NOSTRO and VOSTRO Accounts?

Here is a table describing the difference in NOSTRO vs VOSTRO accounts in detail.

| Aspect | NOSTRO | VOSTRO |

|---|---|---|

| Currency | A NOSTRO account meaning, held in foreign currency by the domestic bank | Held in local currency by the domestic bank |

| Ownership | Owned and maintained by the foreign bank | Owned and maintained by the domestic bank |

| Purpose | Facilitates local transactions for the foreign bank | Enables foreign banks to conduct transactions locally |

| Transactions | Facilitates foreign bank transactions in the host country | Facilitates foreign banks to conduct transactions in local markets where they lack a presence |

| Accessibility | Enhances international financial operations | Provides foreign banks with access to local markets without establishing a direct presence |

Redirecting to Another Bank - Optimising Processing Speed

Banks strive to create effective and speedy foreign currency processing as it contributes to more customers who execute cross-border transactions. However, there may be some technical, regulatory, or geographical restrictions for the bank to have a slow foreign currency processing time. In such cases, banks redirect the transactions to other banks to optimise the processing speed, called transaction redirection.

The primary objective is to achieve faster, more cost-effective, and more reliable settlement while leveraging the capabilities and networks of other banks or intermediaries. Transaction redirection works on correspondent relationships principle with other global banks and financial institutions.Transaction redirection often involves utilising NOSTRO accounts to optimise the processing of cross-border transactions.

For example, let’s say you request Bank A in your country to make a certain payment to a foreign beneficiary. To fulfil the payment request, Bank A can redirect the payment transaction to the correspondent bank's NOSTRO account and instruct the bank to debit the NOSTRO account with the funds and credit them into the recipient’s account.

Transaction redirection streamlines foreign currency payments by leveraging the correspondent bank’s technical infrastructure and NOSTRO accounts to ensure quick payment processing. Transaction redirection can help mitigate risks associated with currency fluctuations, settlement failures, and regulatory compliance.However, some correspondent banks may charge fees for processing transactions through their NOSTRO accounts, which can negate potential cost savings. Furthermore, relying on correspondent banks for transaction redirection introduces counterparty risk. If the correspondent bank encounters financial difficulties or becomes insolvent, it can disrupt transaction processing and potentially lead to losses.

Future Trends in Foreign Currency Processing

Global economies are witnessing a shift to digital technologies, revolutionising how individuals or companies do business. A significant contributor to the success of global businesses is the foreign currency processing time, which makes or breaks the cross-border transactional system.

The ongoing efforts to improve international remittance transfers have also garnered the attention of leaders from major economies, international financial institutions (IFIs), and standard-setting bodies (SSBs).

Their primary goal is to simplify and reduce the costs of sending remittances, a crucial issue in the global development agenda. This commitment to reform began in the early 2000s, with the G8 and G20 groups taking significant steps and committing to cut costs.

Even the United Nations (UN) included reducing remittance expenses as a target within the Sustainable Development Goals (SDGs).

Recent developments, such as the G20 Roadmap in collaboration with IFIs, SSBs, and central banks, are aimed at lowering the expenses of cross-border payments, including remittances and enhancing the transparency, accessibility, and transaction speed of these international financial transactions.

Alongside these reforms, the Financial Action Task Force (FATF) is conducting a review to identify areas where differing anti-money laundering and counter-terrorism financing regulations or their implementation might hinder the efficiency of cross-border payments, especially in the remittance market.

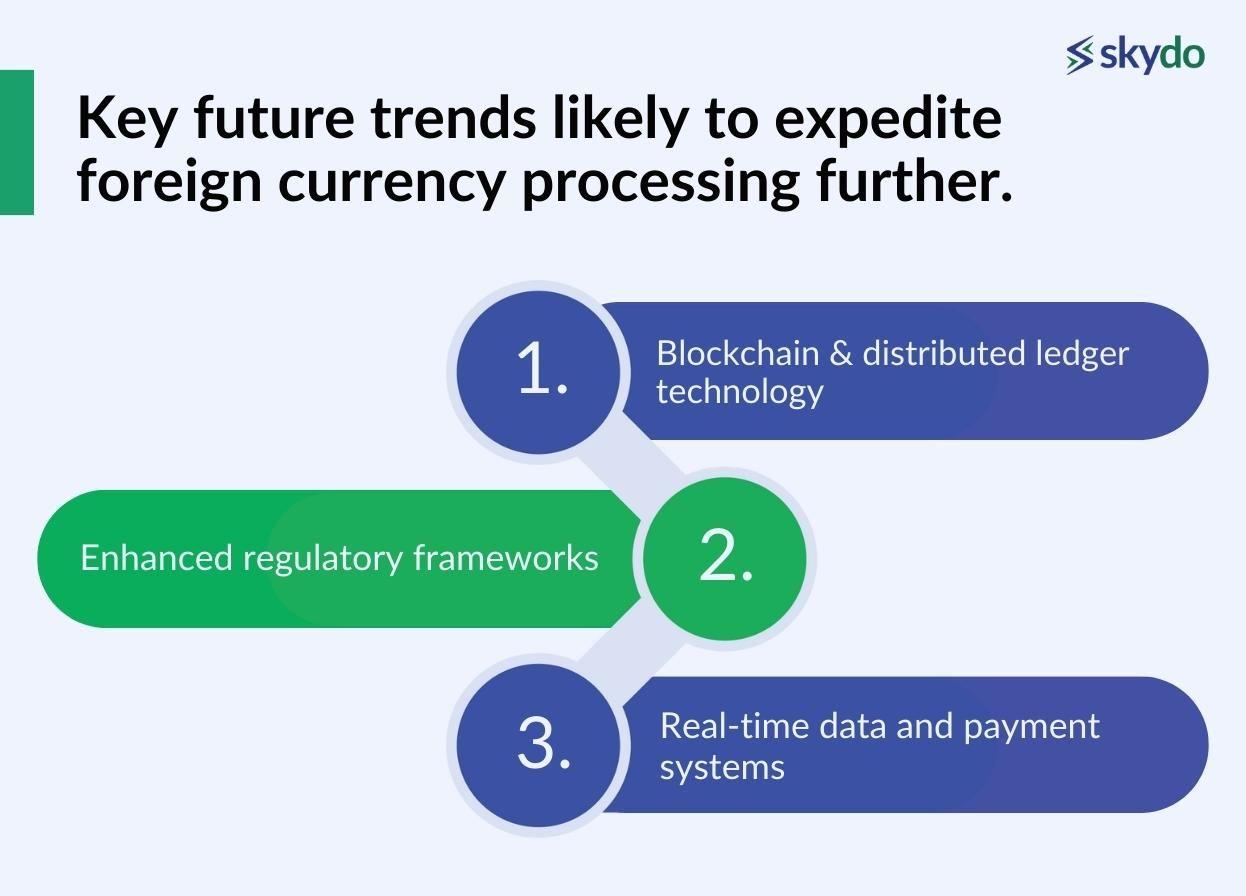

Here are some key future trends likely to expedite foreign currency processing further.

1. Blockchain and distributed ledger technology

Blockchain and DLT offer a secure and transparent ledger to record and verify foreign currency transactions. Leveraging blockchain and DLT can significantly lower the foreign currency processing time and cost by providing real-time settlement and removing the need for intermediaries.

2. Real-time data and payment systems

Digital cross-country payments are increasing in volume with each passing day, and most countries are upgrading their payment systems. The upgrade focuses on integrating advanced technologies such as APIs (Application Programming Interface) and payment systems such as RTGS (Real-Time Gross Settlement) to enhance the speed and efficiency of foreign currency processing.

3. Enhanced regulatory frameworks

Most countries, including India, are looking to update and amend the rules of foreign currency transactions. For example, the Ministry of Finance recently amended FEMA to bring International Credit Card payments by resident Indians outside India within the LRS limit of USD 2.5 lakhs. Such enhanced regulatory frameworks promote innovation in the cross-border financial sector and enhance transaction tracking, transparency, and speed.

Conclusion

The introduction of NOSTRO accounts by AD-1 category banks has proven to be a game-changer in facilitating the seamless execution of cross-border payments. These accounts act as liquidity buffers, ensuring banks have sufficient foreign currency to process international transactions efficiently. NOSTRO accounts, often integrated with the SWIFT messaging system, enable real-time or near-real-time settlement of these transactions.

Looking ahead, the landscape of foreign currency processing is poised for further transformation. Emerging technologies like blockchain and distributed ledger technology promise heightened security and transparency, while real-time data and payment systems are set to revolutionise the speed and efficiency of cross-border transactions. Enhanced regulatory frameworks, aimed at promoting innovation and transparency, are also on the horizon.

As global economies continue to evolve and digital technologies reshape the business landscape, the future of foreign currency processing holds the promise of faster, more cost-effective, and more transparent cross-border transactions. These developments are not only reshaping the way we conduct international business but also have far-reaching implications for the stability of the global financial system and the growth of economies worldwide.

Frequently Asked Questions

Q1. What is a NOSTRO account in banking?

Ans: A NOSTRO account in banking is a foreign currency account held by a domestic bank in another financial institution, typically in the country's currency where the foreign bank is located.

Q2. Why is a NOSTRO account required?

Ans: A NOSTRO account is required to facilitate international transactions, allowing banks to hold foreign currency for smoother cross-border payments and settlements.

Q3. What is NOSTRO, VOSTRO, and LORO account?

Ans: NOSTRO, VOSTRO, and LORO accounts refer to accounts held by one bank in another. NOSTRO is the foreign account held by a domestic bank, VOSTRO is the local account held by a foreign bank, and LORO is an account held by an intermediary bank on behalf of others.

Q4. How to perform NOSTRO reconciliation?

Ans: NOSTRO reconciliation involves comparing and matching a bank's NOSTRO account records with its corresponding banks to ensure accurate and error-free transactions.

Q5. What is the difference between NOSTRO and VOSTRO accounts?

Ans: The main difference between NOSTRO and VOSTRO accounts lies in perspective: NOSTRO is the foreign account from the home bank's viewpoint, while VOSTRO is the local account from the foreign bank's viewpoint.

Q6. How to open a NOSTRO account?

Ans: To open a NOSTRO account, a bank typically establishes relationships with correspondent banks abroad, following due diligence and compliance with regulatory requirements.

Q7. Which bank is best for international transactions?

Ans: The best bank for international transactions depends on fees, exchange rates, and network coverage; popular choices include HSBC, Citibank, and JPMorgan.

Q8. How do I transfer money to my NOSTRO account?

Ans: A NOSTRO account is a bank service and not an account that an individual owns. If you want to transfer a certain amount in foreign currency, your bank will do the needful through their NOSTRO account, ensuring that funds are available in foreign currency.

Q9. What is the purpose of a NOSTRO account?

Ans: The purpose of a NOSTRO account is to facilitate international trade and transactions by holding foreign currency and streamlining cross-border payments and settlements.

Q10. In which currency is the NOSTRO account available?

Ans: NOSTRO accounts are available in various foreign currencies, depending on the needs and preferences of the bank, such as USD, EUR, GBP, etc.