Fedwire vs. ACH: Choosing the Right Payment Method in India

Among various electronic payment systems, two prominent players in the United States are Fedwire and the Automated Clearing House (ACH) network. While both facilitate electronic fund transfers, understanding Fedwire vs ACH is crucial for deciding about which system best suits specific financial needs.

This blog will help you understand everything about ACH Vs Fedwire and help you choose the most suitable payment system.

What is Fedwire?

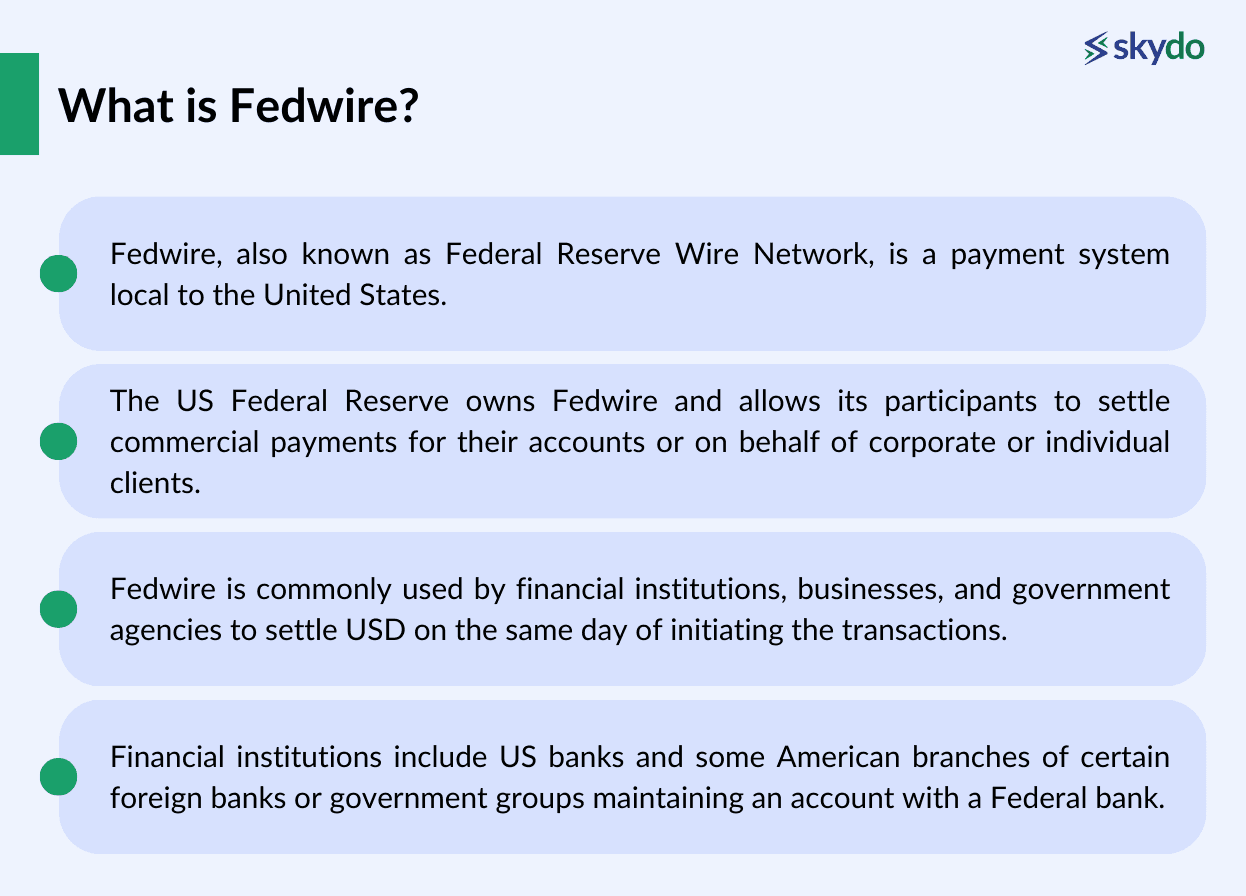

Fedwire, also known as Federal Reserve Wire Network, is a payment system local to the United States, allowing entities to execute time-sensitive, large-value transactions. Fedwire is a well-known payment network for entities as it processes transactions in real-time (immediate fund transfers) with high transactional security.

The US Federal Reserve owns Fedwire and allows its participants to settle commercial payments for their accounts or on behalf of corporate or individual clients. Fedwire can also be used to settle positions with banks and other financial institutions, buy and sell federal funds, or submit federal taxes.

Fedwire is commonly used by financial institutions, businesses, and government agencies to settle USD on the same day of initiating the transactions. Financial institutions include US banks and some American branches of certain foreign banks or government groups maintaining an account with a Federal bank.

What is ACH?

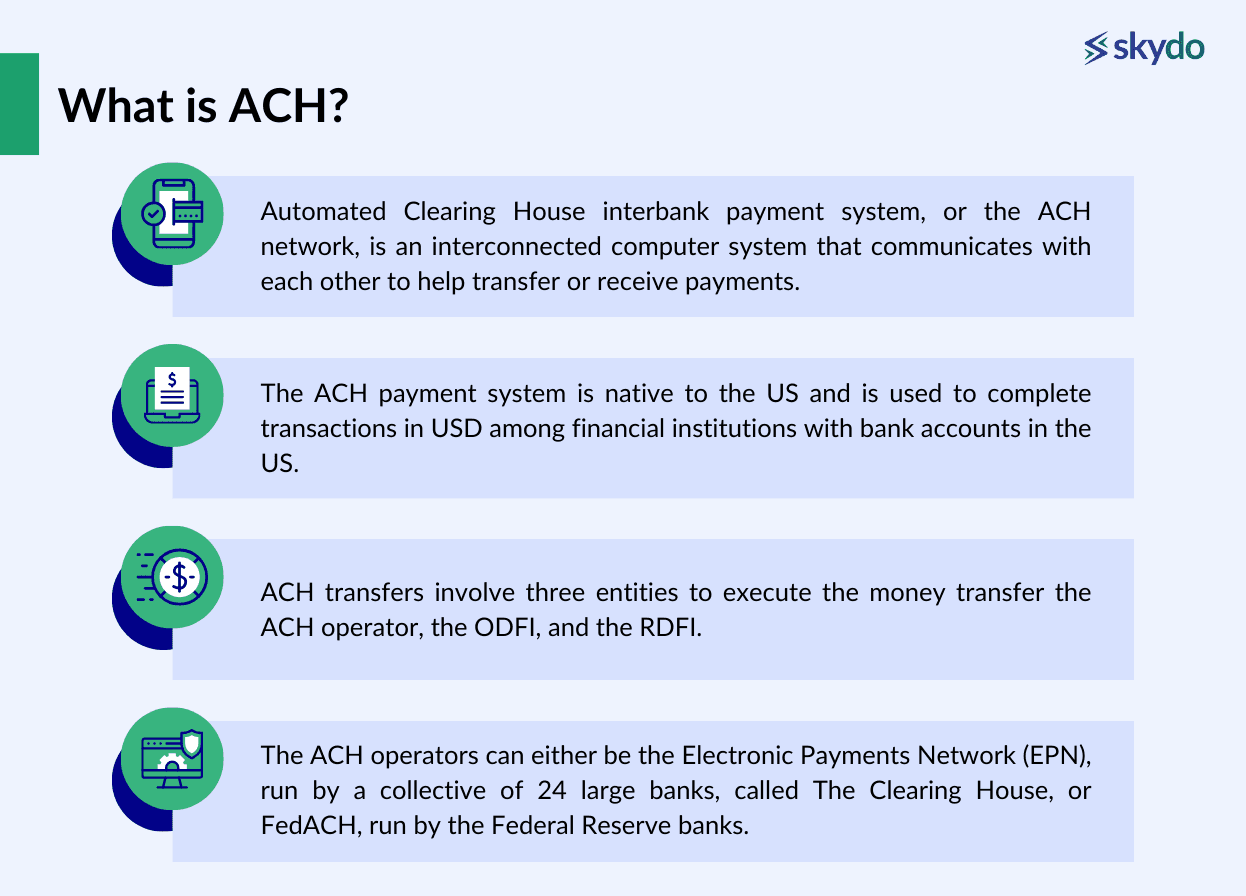

Automated Clearing House interbank payment system, or the ACH network, is an interconnected computer system that communicates with each other to help transfer or receive payments. The ACH payment system is native to the US and is used to complete transactions in USD among financial institutions with bank accounts in the US.

ACH payments do not restrict themselves to transferring person-to-person money, but individuals can use the ACH network to pay bills online, pay salaries to employees, pay mortgages and loans, and for tax refunds or payments.

ACH transfers involve three entities to execute the money transfer- the ACH operator, the ODFI, and the RDFI. The ACH operators can either be the Electronic Payments Network (EPN), run by a collective of 24 large banks, called The Clearing House, or FedACH, run by the Federal Reserve banks.

ACH is an open and inclusive system that allows various financial institutions to participate. This includes commercial banks, credit unions, savings banks, and other financial entities. As a result, ACH has become a standardised and universally accepted platform for electronic funds transfer.

Choosing the Right Method

Here is a detailed comparison between Fedwire and ACH transactions to help you choose the right method based on factors such as transaction amount, payment urgency, security, transfer frequency, and transaction limitations.

| Particulars | Fedwire | ACH |

|---|---|---|

| Transaction Limit | Large value transactions with a transaction limit of $9,999,999,999.99. | Lower-value transactions range from $3,500 to $25,000 per day. |

| Payment Type | Domestic and international payments for certain foreign branches within the US | Domestic transactions within the US |

| Transaction Speed | Real-time gross settlement (RTGS) instantly or within a few hours | Transaction settlement between three to five business days |

| Transaction Cost | Higher transaction costs for customers ranging between $35-$50 per transaction | Lower transaction costs compared to Fedwire |

| Security | Highly secure, negligible chances of financial fraud | Relatively secure but includes chances of financial fraud |

| Participants | No need for a third party to execute transactions, resulting in quicker transactions | Relies on a third party, called the clearing house, to complete transactions, resulting in longer transaction settlements |

| Operating Hours | Available on weekdays from 9 p.m. the prior calendar day to 7 p.m. | Available 23¼ hours every business day and settles payments four times a day. |

| Transaction Confirmation | Immediate acknowledgement | Delayed confirmation, not in real-time |

| Common Use Cases | High-value, time-sensitive transactions | Recurring payments, payroll, bill payments, etc. |

| Currency Support | Primarily deals with USD | Support other currencies through Multi-currency ACH |

| Accessibility for Small Institutions | Primarily for larger financial institutions executing high-value transactions | Accessible to both large and small institutions, often through third-party providers |

Conclusion

Fedwire and ACH are two prominent payment systems in the United States, each with its unique features and purposes. Fedwire excels in real-time settlement of high-value transactions, while ACH offers a versatile and cost-effective solution for various payment types, albeit with a longer processing time.

Choosing the appropriate payment method is crucial, depending on the specific needs of the transaction. Fedwire's real-time settlement makes it a preferred choice for urgent and large-value transactions. On the other hand, ACH is ideal for recurring payments, payroll, and other non-time-sensitive transactions.

However, it is crucial for individuals and businesses to carefully consider the characteristics of each system and select the payment method that aligns with their specific requirements. Researching additional details or consulting with an expert can provide valuable insights and guidance on making informed financial and transactional decisions.

FAQs

Q1. Is Fedwire different from wire transfer?

Ans: Fedwire is one of the most widely used wire transfer methods in the United States. However, it is not the same as wire transfer, as it is a broader term that refers to the electronic transfer of funds from one financial institution to another. Wire transfers can take various forms, and they are not limited to a specific system or network.

Q2. What is the difference between ACH, Fedwire, and SWIFT?

Ans: Although all of these are payment networks in the US, they differ in numerous factors such as transaction speed, transaction cost, processing times, etc. An example is that ACH takes 3-4 business days, SWIFT takes up to 5 business days, and Fedwire settles the transaction instantly.

Q3. What type of payment is Fedwire?

Ans: Fedwire is an electronic payment system known as a Real-Time Gross Settlement (RTGS) system. In an RTGS system like Fedwire, transactions are settled immediately and individually.

Q4. Which is faster ACH or wire transfer?

Ans: Wire transfers are faster as they work on the Real-Time Gross Settlement (RTGS) system, settling transactions instantly. In comparison, ACH transfers (if not same-day ACH) take up to 3-4 business days to settle.