How Long Do International Wire Transfers Take?

Cash flow is the lifeblood of any business, and late cross-border payments can bleed through your operational costs. From missed opportunities to strained relationships, delays in foreign or inward remittances have a significant impact.

This blog unpacks the payment system intricacies across key markets, to help you navigate the global payment maze and avoid costly delays.

Time Taken For Inward Remittances Worldwide

The central banks of various countries have set frameworks and policies to ensure seamless and secure financial transactions. Like India’s NEFT and RTGS, major countries have their payment networks with distinctive processing times and cost structures.

Here are the major countrywide payment systems with their processing times.

Time Taken by ACH Payments

Automated Clearing House, or the ACH network, is an interconnected computer system that communicates with each other to help transfer or receive payments within the US.

The ACH network has evolved from person-to-person payments to allow individuals to utilise the network to make bill payments, pay salaries to employees or make mortgage repayments.

The National Automated Clearing House, or NACH, governs the payments executed through the ACH network.

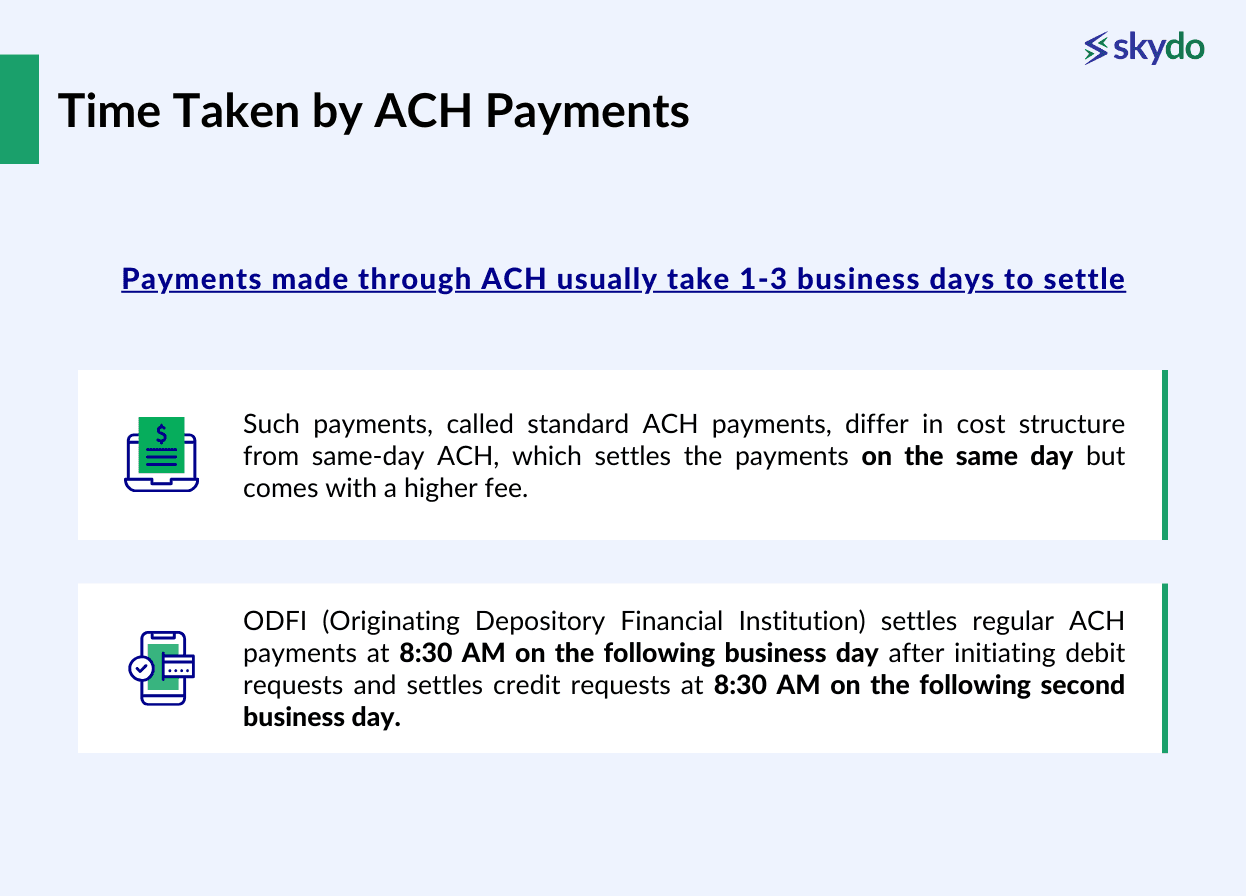

Payments made through ACH usually take 1-3 business days to settle. Such payments, called standard ACH payments, differ in cost structure from same-day ACH, which settles the payments on the same day but comes with a higher fee.

ODFI (Originating Depository Financial Institution) settles regular ACH payments at 8:30 AM on the following business day after initiating debit requests and settles credit requests at 8:30 AM on the following second business day.

Time Taken by FPS Payments

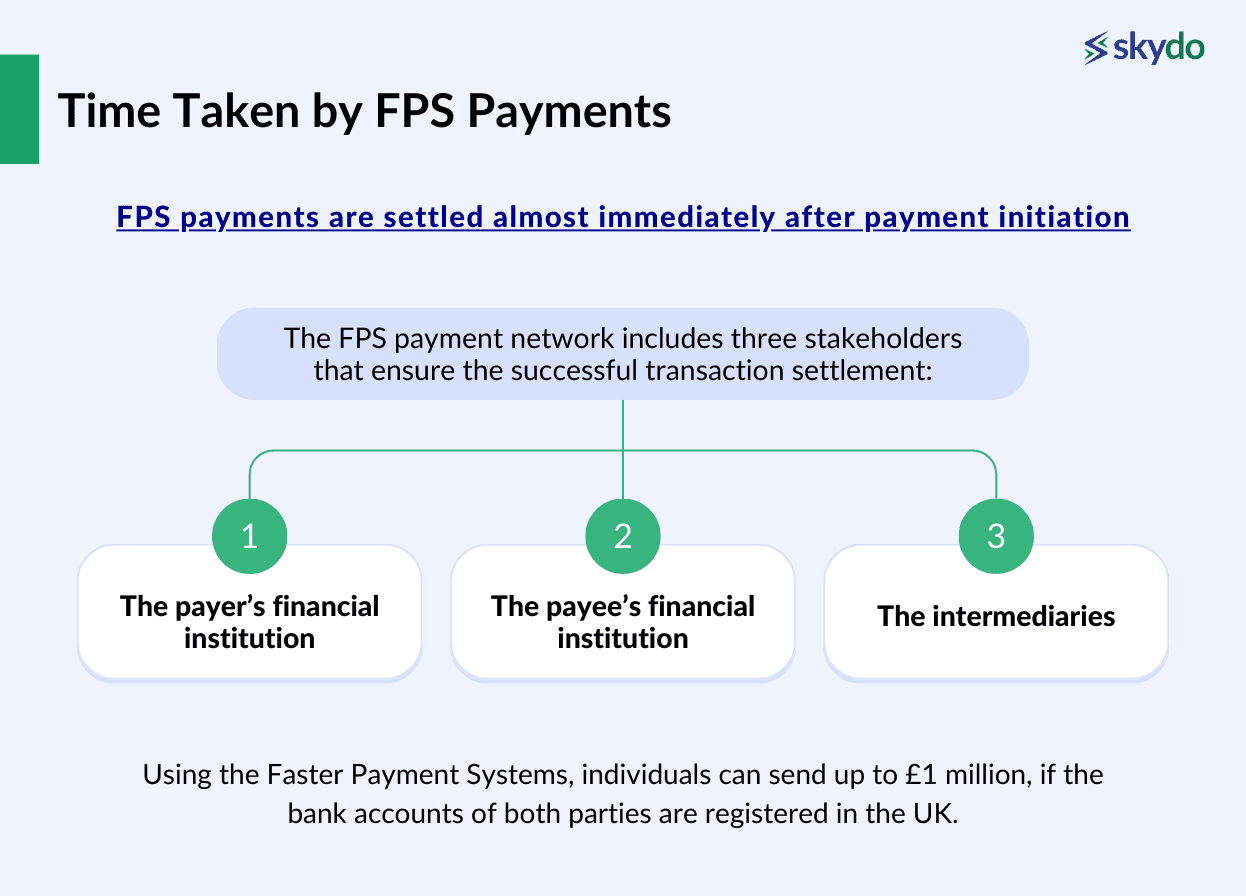

The Faster Payments Service (FPS) allows the settling of digital financial transactions between two bank accounts registered in the UK. The FPS payment network includes three stakeholders that ensure the successful transaction settlement:

- The payer’s financial institution

- The payee’s financial institution

- The intermediaries

Using the Faster Payment Systems, individuals can send up to £1 million, if the bank accounts of both parties are registered in the UK.

FPS payments are settled almost immediately after payment initiation. However, some payments may take up to two hours. Although the upper limit is £1 million, banks set their limit for the maximum amount entities can send per transaction or daily using FPS.

Unlike ACH, which carries an average cost of $0.29 per transaction, FPS payments are free for retail customers but carry a fee of around £2.50 per transaction for corporate customers.

Time Taken by SEPA Payments

SEPA, or The Single Euro Payments Area, is a payment network to send and receive payments electronically within Europe. The transfer happens in Euros between two banks or financial institutions in the Eurozone (European region).

Thirty-six countries are members of the SEPA network, and the two bank accounts should be registered in any of the member countries for the SEPA transfers to be completed.

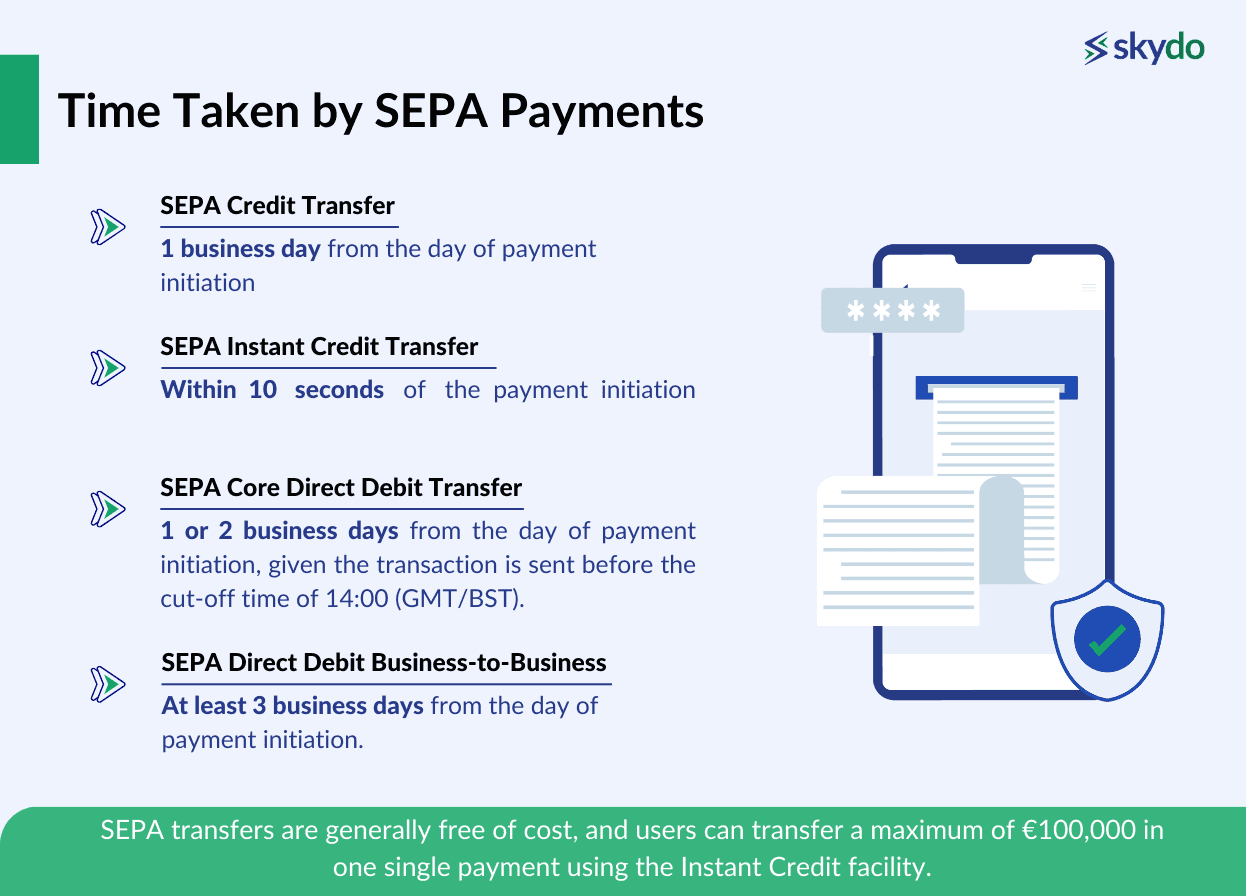

SEPA transfers are generally free of cost, and users can transfer a maximum of €100,000 in one single payment using the Instant Credit facility.

The processing time for SEPA transactions differs based on the four types of payment processing schemes, which are;

- SEPA Credit Transfer: 1 business day from the day of payment initiation.

- SEPA Instant Credit Transfer: Within 10 seconds of the payment initiation.

- SEPA Core Direct Debit Transfer: 1 or 2 business days from the day of payment initiation, given the transaction is sent before the cut-off time of 14:00 (GMT/BST).

- SEPA Direct Debit Business-to-Business: At least 3 business days from the day of payment initiation.

Time Taken by AFT Payments

Similar to the US, ACH payment networks also allow settling funds in CAD within two bank accounts in Canada. Canada AFT (Automated Fund Transfer) is another cost-effective and convenient solution.

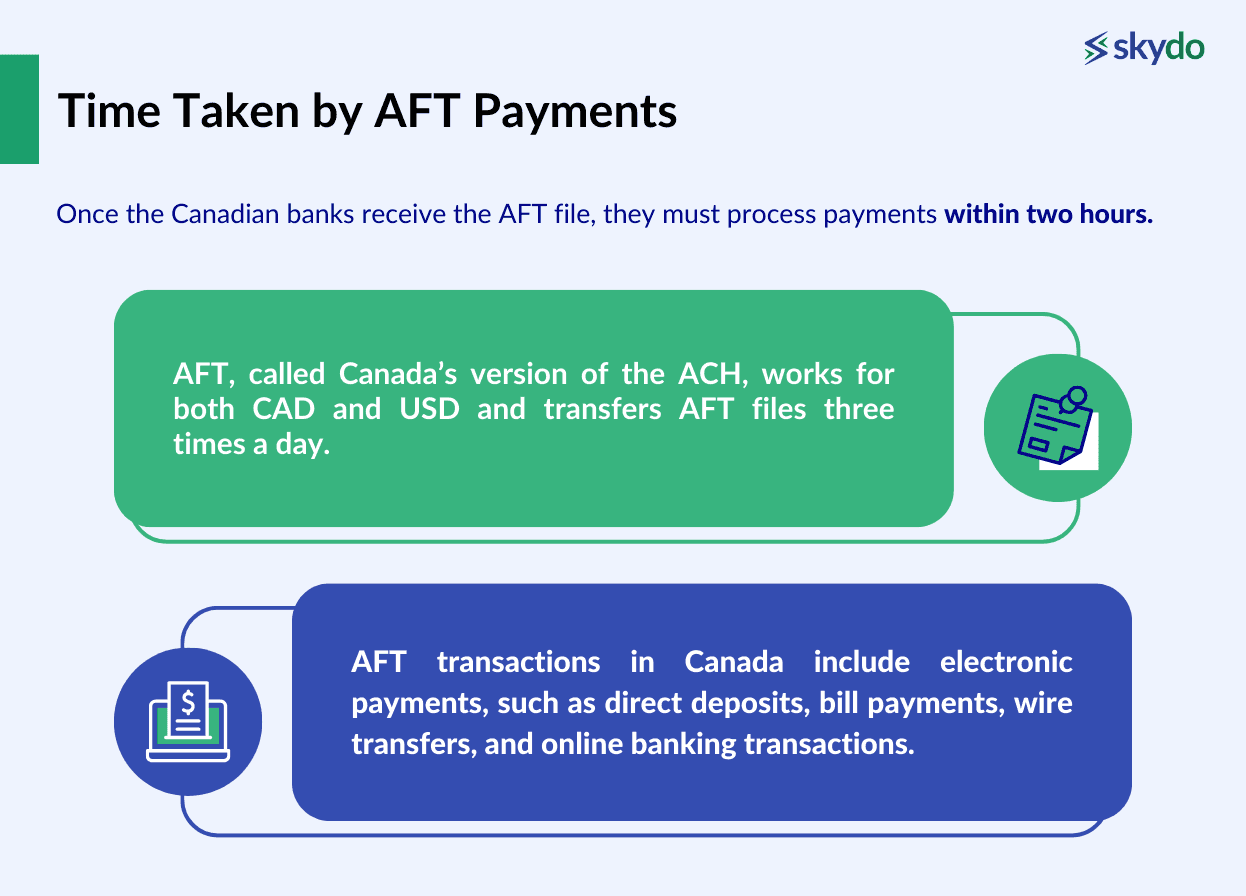

AFT, called Canada’s version of the ACH, works for both CAD and USD and transfers AFT files three times a day. Once the Canadian banks receive the AFT file, they must process payments within two hours.

AFT transactions in Canada include electronic payments, such as direct deposits, bill payments, wire transfers, and online banking transactions. Canadian Payments Association (now part of Payments Canada) oversees and facilitates the electronic payment systems in the country.

Time Taken by NPP

The New Payments Platform (NPP) was launched in February 2018 as an open-access infrastructure for executing fast payments within Australia.

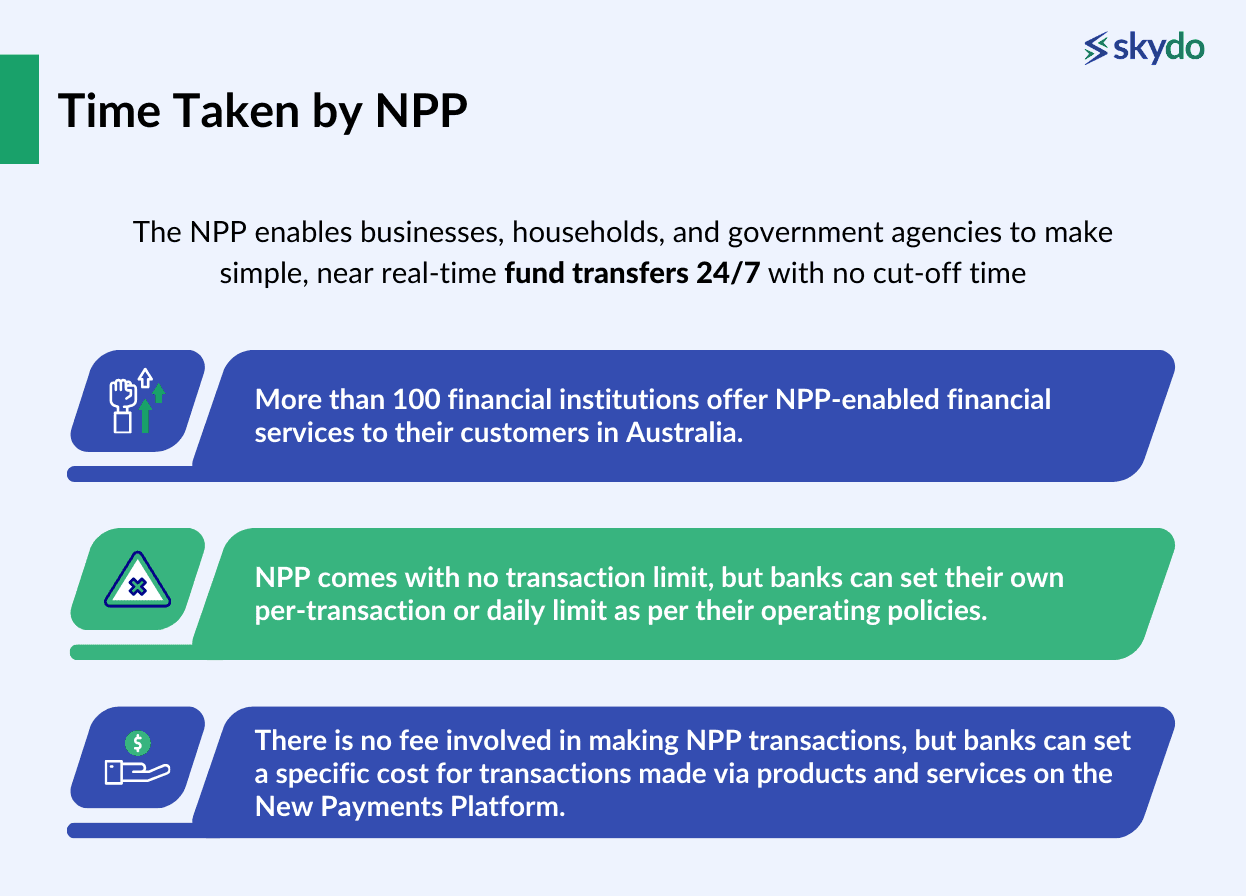

The NPP enables businesses, households, and government agencies to make simple, near real-time fund transfers 24/7 with no cut-off time. NPP differs from other payment networks as it carries much richer remittance information with each payment message.

In 2022, NPP merged with BPAY Group and EFTPOS to form the Australian Payment Plus. More than 100 financial institutions offer NPP-enabled financial services to their customers in Australia.

NPP comes with no transaction limit, but banks can set their own per-transaction or daily limit as per their operating policies. There is no fee involved in making NPP transactions, but banks can set a specific cost for transactions made via products and services on the New Payments Platform.

Time is Money: Choosing the Right Tool

Before choosing the right payment network, you should compare them based on the urgency of transaction settlement, amount, sender/receiver location, and fee.

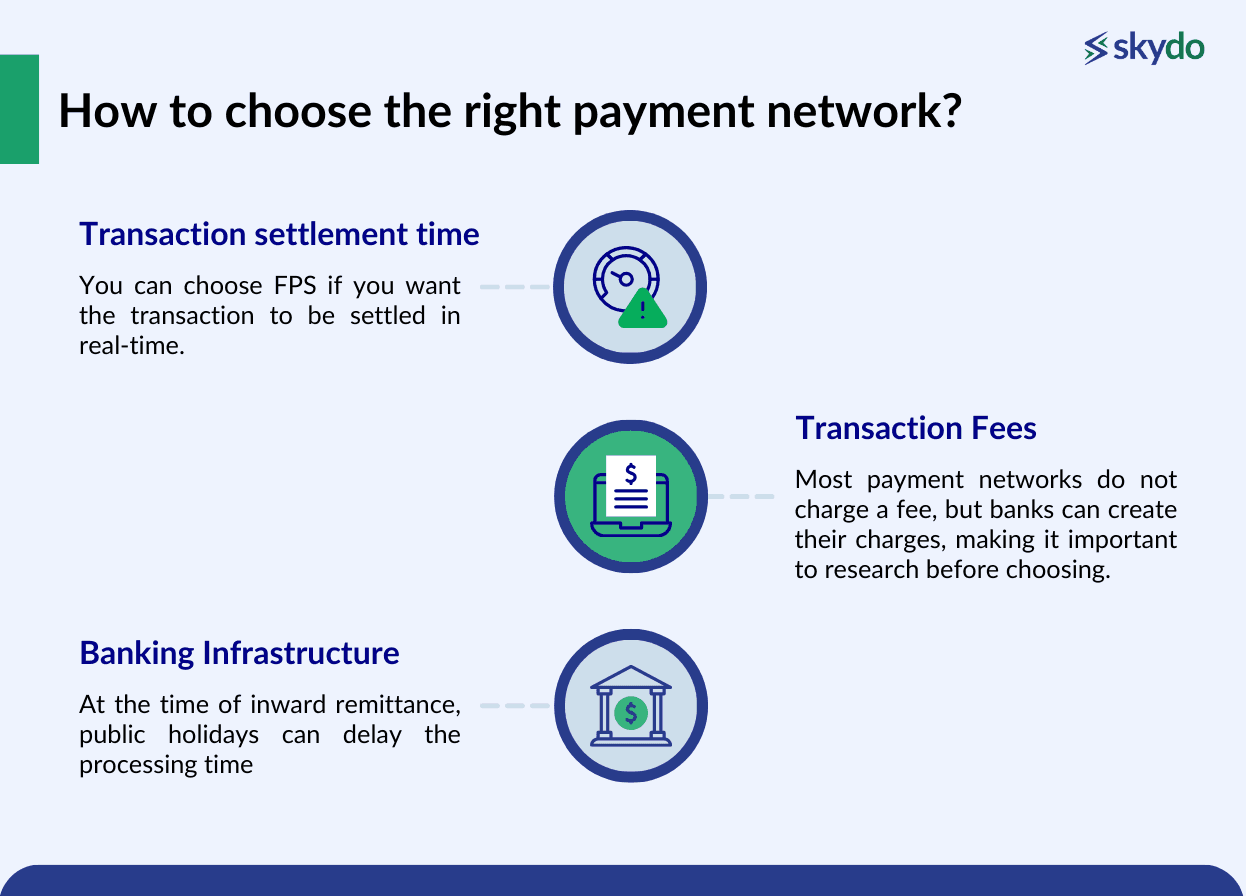

- Transaction settlement time

You can choose FPS if you want the transaction to be settled in real-time. However, you can choose SEPA transfers if you want to transfer a high amount.

Furthermore, you must consider the location of the receiver or the sender as most payment networks require bank accounts registered within the same region.

- Transaction Fees

Most payment networks do not charge a fee, but banks can create their charges, making it important to research before choosing.

- Banking Infrastructure

At the time of inward remittance, public holidays can delay the processing time. As intermediary banks communicate with each other to complete payments, their technical infrastructure also affects payment processing.

Most individuals who don’t have a bank account in the same region utilise alternative inward remittance options such as money transfer services, international debit cards, or international payment platforms such as Stripe and Skydo.

How to Minimise Payment Delays?

Ensure that all recipient information is accurate and complete. Double-check the recipient's name, address, account number, and any other required details.

Initiate remittance transactions well in advance, especially if specific deadlines or time-sensitive requirements exist. Stay informed about the regulatory requirements for inward remittances in both the sending and receiving countries.

Maintaining open lines of communication with both the sender and recipient and any intermediaries involved in the process can also prove ideal in avoiding processing delays.

Conclusion

Understanding the nuances of remittance worldwide is vital for seamless business transactions, as most countries have payment networks similar to India’s RTGS or NEFT. As these payment networks differ in their processing time and cost structure, they can significantly affect the time taken for inward remittances.

Accuracy in recipient information, early initiation of transactions, and a comprehensive understanding of compliance checks form the foundation for minimising delays. Furthermore, it is vital to analyse and compare the payment networks based on factors such as transfer amount, urgency, and the requirement for bank accounts.

FAQs

Q1. Who is the remitter in banking?

Ans: Remitter meaning in bank refers to the individual or entity that is sending or initiating a remittance. The remitter could be an individual sending money to family members, a business making international payments, or anyone involved in the process of transferring funds across borders.

Q2. What fees are associated with cross-border payments?

Ans: There are numerous costs associated with cross-border transactions, such as bank fees, transfer fees, currency conversion fees, exchange fees, international money transfer platform fees, and international debit or credit card fees.

Q3. What are the most common payment methods for international transactions?

Ans: The most common payment methods include wire transfers, international debit/credit cards, and online payment platforms.