What is an Overdraft Facility? Its Types, Benefits and Eligibility

OD covers short-term gaps. Skydo helps you avoid them by settling export proceeds in 24 hours with FIRA included.

Meet Mr Anshul Mehta, an IT service exporter, currently facing a cash crunch due to delayed payments from his international clients. These delayed payments have affected his liquidity, making it challenging for him to pay salaries to his staff and fulfil his tax obligations on time. In this difficult situation, Mr Mehta uses his bank's overdraft facility to address his short-term capital requirements effectively.

What Is an OD Facility?

The bank overdraft facility is a valuable tool for Mr Mehta to manage his short-term capital requirements during this period of cash crunch. It allows him to bridge the gap between delayed payments and essential financial obligations without disrupting his business operations.

In times of financial difficulty, a bank overdraft facility can be a lifesaver for businesses like Mr Mehta's. It provides a flexible and approved line of credit to address short-term capital requirements, allowing entrepreneurs to manage their financial obligations efficiently.

By judiciously utilising such facilities, businesses can navigate challenging times and ensure continuity and growth.

Revenue Leak Calculator

- ✓ Fees quietly eating margin?

- ✓ Current provider vs Skydo

- ✓ Reclaim what's yours

How Does the OD Facility Work?

The Overdraft Facility allows you to withdraw money over the amount available in your bank account within the specified limit. This means you can use an overdraft facility even if your account has zero balance. It is a short-term credit agreement to help you meet more immediate or direct capital requirements.

The scope of the overdraft facility depends on the credit limit pre-sanctioned by the bank based on its relationship with the customer. You can withdraw small amounts of money or the entire credit limit together. An overdraft facility differs from a business loan as you are charged interest only on the amount you withdraw, not the total sanctioned credit limit.

Overdraft interest rates may vary from one bank to another. Banks also levy OD charges for non-maintenance of the account. While there are no prepayment penalties, banks may charge you increased interest rates if you default on your payments.

The repayment duration is 12 months, compared to a business loan, which can extend to 10 years. You can repay in a lump sum amount or instalments, unlike loans with regular EMIs to be paid over a fixed tenure.

Mostly, all financial institutions in India provide an overdraft facility to their customers. However, the amount and rate of interest depends upon several factors, such as–

- The borrower’s profile

- Credit score rating and financial history

- Relationship with the bank

- Repayment capacity

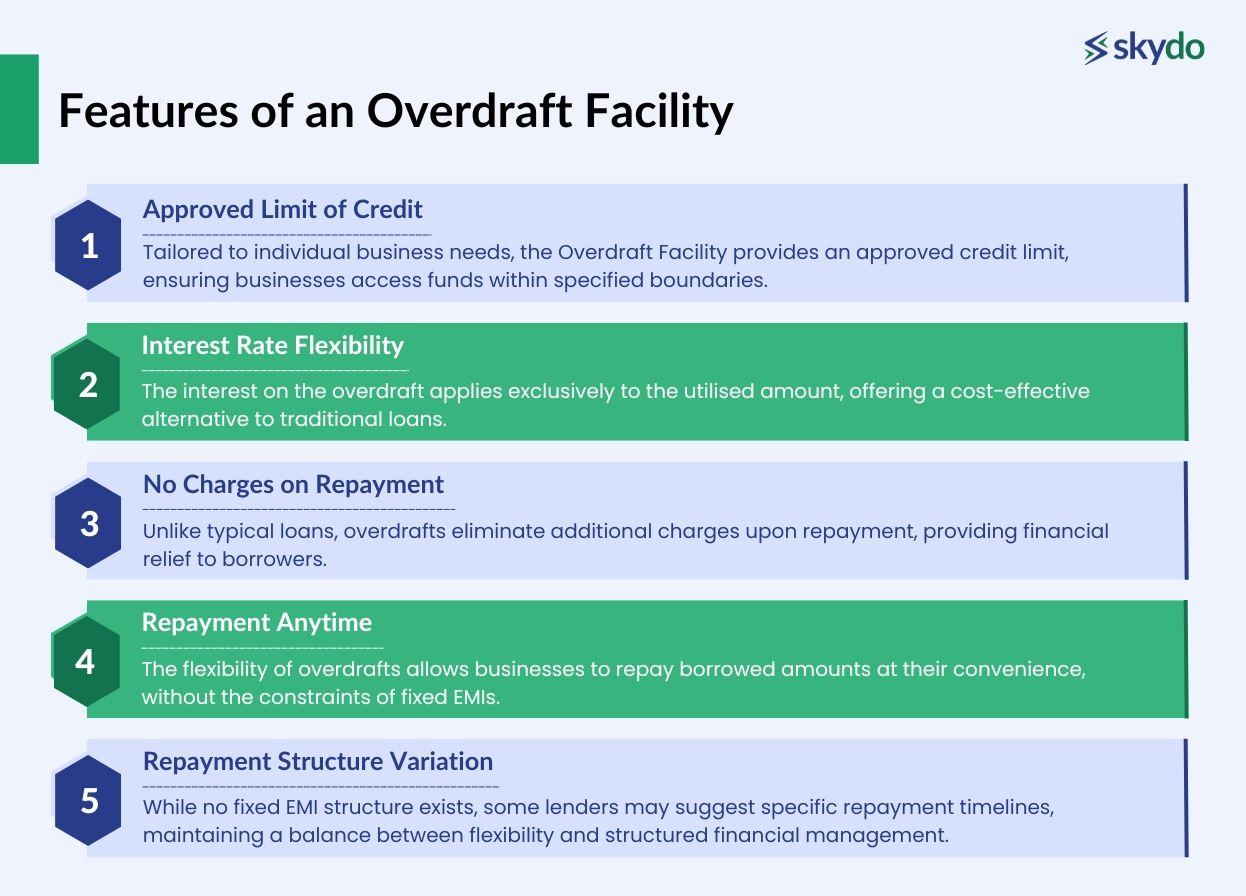

Features of an Overdraft Facility

An Overdraft Facility includes several key features tailored to provide flexibility and financial convenience, such as–

- Approved Limit of Credit: Tailored to individual business needs, the Overdraft Facility provides an approved credit limit, ensuring businesses access funds within specified boundaries.

- Interest Rate Flexibility: The interest on the overdraft applies exclusively to the utilised amount, offering a cost-effective alternative to traditional loans.

- No Charges on Repayment: Unlike typical loans, overdrafts eliminate additional charges upon repayment, providing financial relief to borrowers.

- Repayment Anytime: The flexibility of overdrafts allows businesses to repay borrowed amounts at their convenience, without the constraints of fixed EMIs.

- Repayment Structure Variation: While no fixed EMI structure exists, some lenders may suggest specific repayment timelines, maintaining a balance between flexibility and structured financial management.

Types of OD Facilities

An overdraft facility can be secured or unsecured.

A secured overdraft can help you access additional funds if you have specific assets, such as property, fixed deposit, insurance policies, and equity investments, to offer as collateral against the overdraft. Unsecured overdrafts allow you to access your bank's sanctioned line of credit without collateral.

The interest rates on unsecured overdraft facilities are higher than secured overdrafts.

Eligibility and Application Process

1. Eligibility Criteria for OD Facility

- Age: Any person between the ages of 21 and 65 years

- Bank account: Applicant must have an account with an existing bank

- Minimum Income threshold: varies from bank to bank

- Credit score: A good credit score is an added advantage

2. Required Documents

- Duly filled-in application form with a passport-size photograph

- Identity proof such as Passport, voter ID card, PAN card, License, Aadhar card

- Address proof such as Passport, Driving License, Voter ID card, and Utility Bills

- Age proof such as a Class X certificate, Passport

- Last 12 months’ bank statement

- Any other document asked by the lender or bank

3. Application Process

If the bank does not offer a pre-approved overdraft limit, you can apply for it with the bank by filling out the official form and furnishing the required documents. You can initiate the application process via internet or mobile banking or by visiting your bank branch.

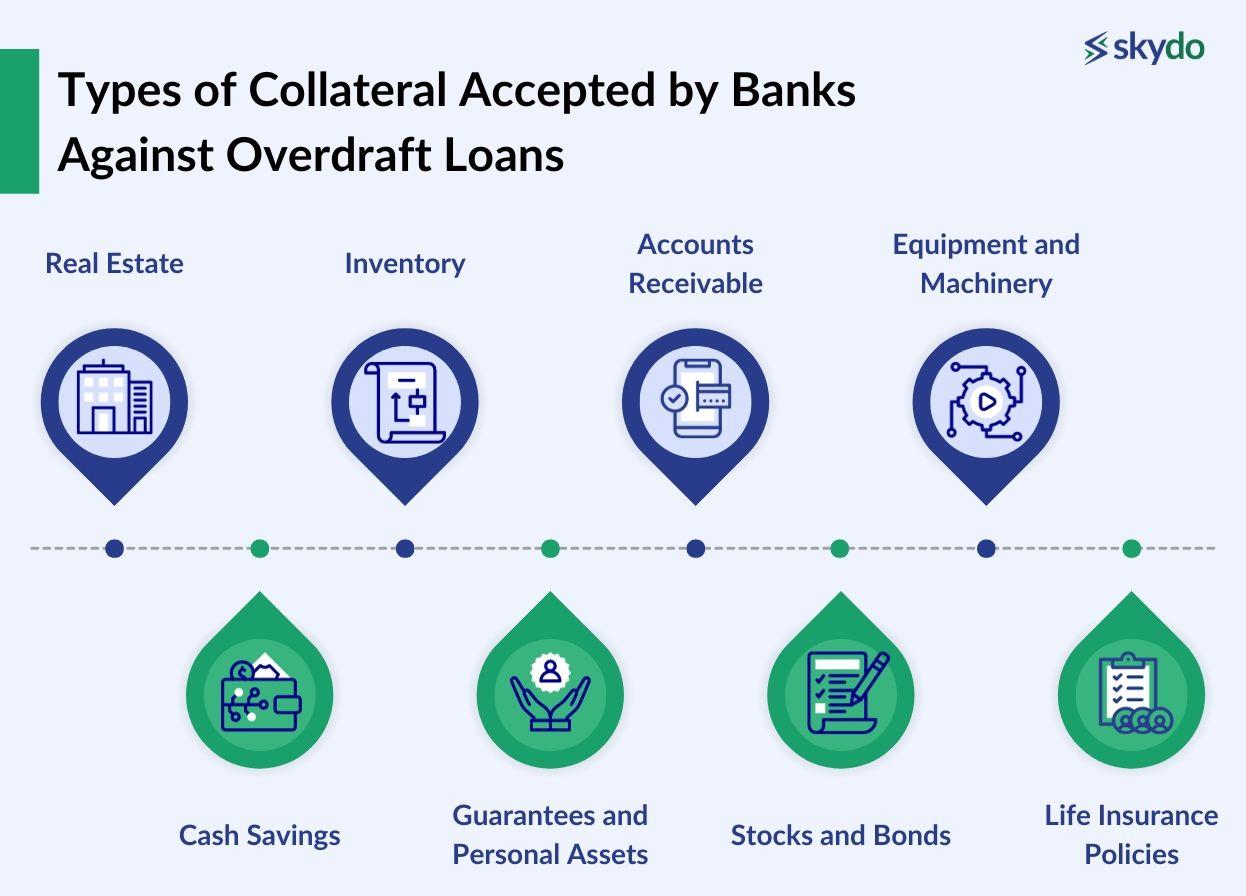

Types of Collateral Accepted by Banks Against Overdraft Loans

Banks typically accept various types of collateral against overdraft loans, providing security for the extended funds. The types of collateral may vary, and the acceptance depends on the bank's policies and the borrower's financial profile.

Here are common types of collateral accepted by banks against overdraft loans.

- Real Estate: Residential or commercial properties can serve as collateral. The bank may assess the property's value and equity to determine the credit limit.

- Inventory: Pledging inventory is common in industries where its value is relatively stable and easily appraised.

- Accounts Receivable: Banks may accept a portion of a business's accounts receivable as collateral. This process, often supported by accounts receivable automation, involves using unpaid customer invoices to secure the overdraft, streamlining collections and improving cash flow efficiency.

- Equipment and Machinery: You can pledge tangible assets such as machinery or equipment. The bank assesses the value and depreciation of these assets to determine their suitability as collateral.

- Cash Savings: Some banks allow borrowers to use their cash savings or certificates of deposit (CDs) as collateral. It provides a straightforward and liquid form of security.

- Guarantees and Personal Assets: Personal guarantees or assets, such as the borrower's personal property or investments, may be accepted as collateral, especially for small businesses or individual borrowers.

- Stocks and Bonds: Marketable securities, such as stocks and bonds, can be used as collateral. The value of these assets may influence the credit limit granted by the bank.

- Life Insurance Policies: Borrowers may pledge the cash value of their life insurance policies as collateral. This is a way to use a personal financial asset to secure business credit.

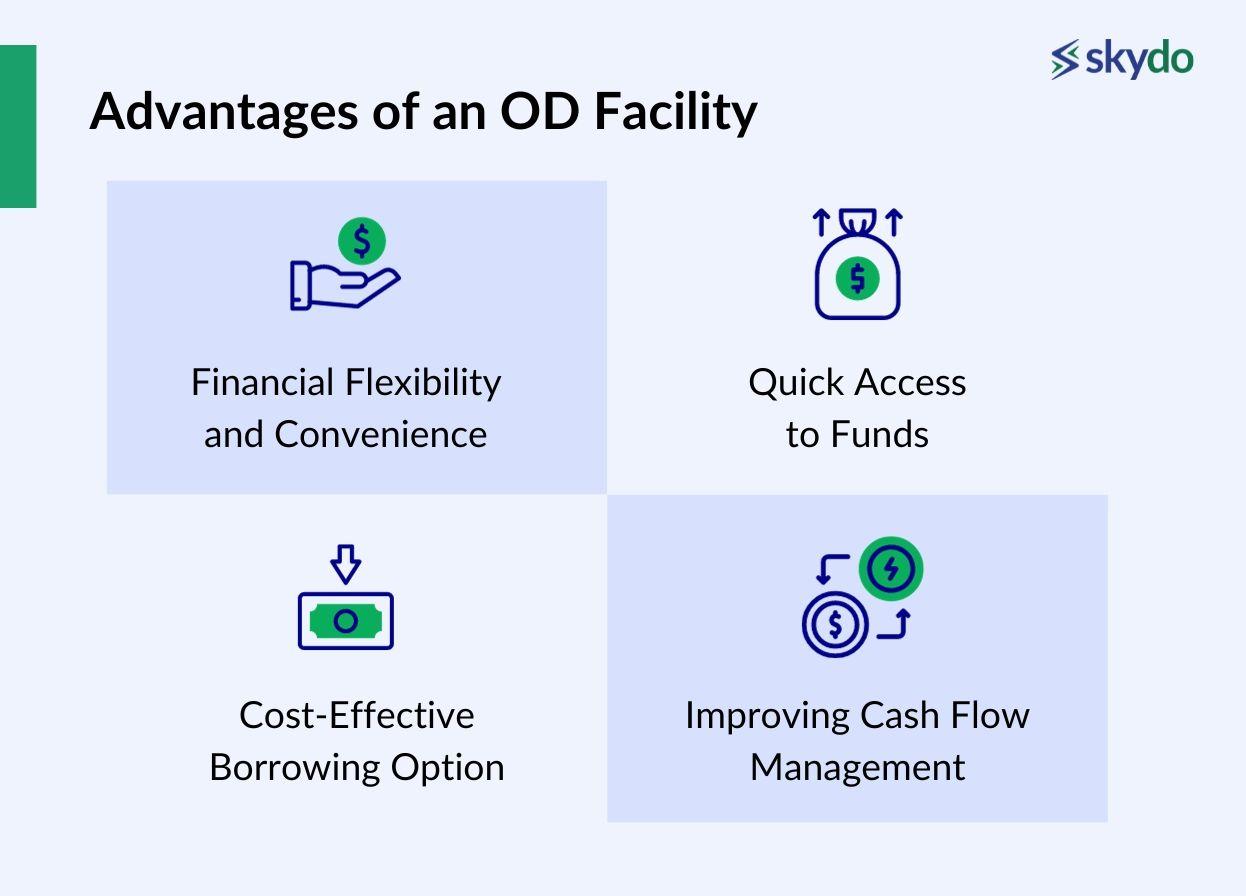

Advantages of an OD Facility

- Financial Flexibility and Convenience: An overdraft facility is a flexible way of accessing short-term credit to meet your immediate business needs. It is further convenient as you don’t need to submit tedious documentation and follow the approval processes in a business loan. The rejection ratio for loans is also higher, while the overdraft facility is readily available with most bank accounts.

- Quick Access to Funds: With an OD facility, you avoid the hassles of procuring a business loan, which can take weeks to get sanctioned and credited to your account. You can avail of the OD facility at any time if you have a bank account with the respective bank.

- Cost-Effective Borrowing Option: The interest rate charged on the overdraft facility is lower than that on a business loan. Additionally, there are no prepayment penalties involved. The interest gets charged only on the amount you withdraw from your bank account, making ODs a cost-effective option to secure quick credit.

- Improving Cash Flow Management: An overdraft facility can provide immediate liquidity to improve overall cash flow management in daily business operations.

Disadvantages of an OD Facility

While an Overdraft (OD) Facility offers financial flexibility, it has some inherent disadvantages.

- High-interest rates, making it a costly form of borrowing

- The absence of a fixed repayment structure

- The OD approval is contingent on a good credit history

- Dependency on overdrafts may mask underlying financial issues, hindering long-term financial stability.

Careful consideration and financial planning are essential to mitigate these disadvantages and maximise the benefits of an OD Facility.

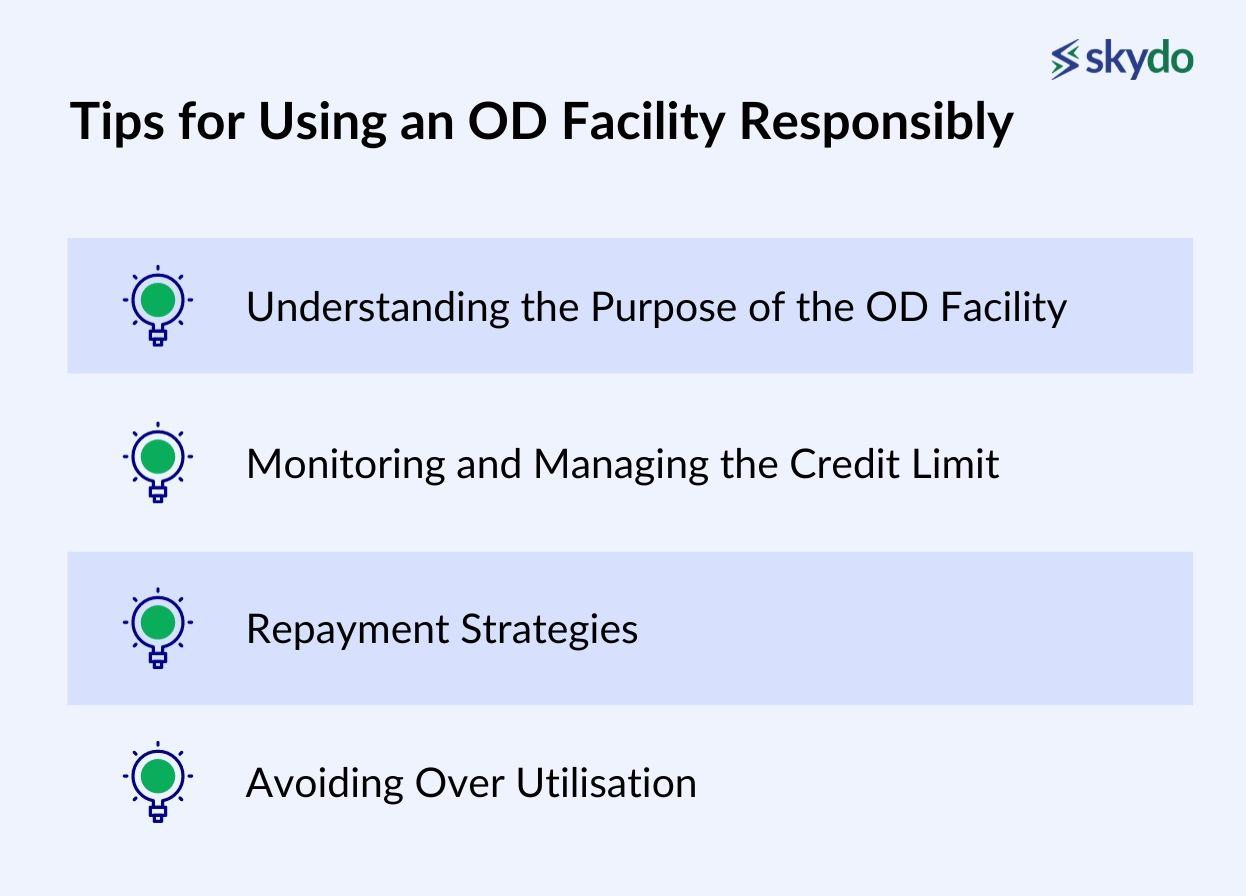

Tips for Using an OD Facility Responsibly

- Understanding the Purpose of the OD Facility: An overdraft facility allows businesses and individuals to meet urgent credit needs. It is a form of a loan you need to pay with interest. You must use the OD facility only when necessary and comply with the repayments in time.

- Monitoring and Managing the Credit Limit: Banks allow you to increase or decrease the credit limit on your overdraft facility. Keep a strict eye on your credit needs and set a limit accordingly.

- Repayment Strategies: While banks don’t have an instalment system for OD repayment, you still need to repay within a fixed tenure. The interest rates are applicable daily. Therefore, the sooner you finish your OD repayments, the more you save on interest.

- Avoiding Over Utilisation: Withdraw only the required funds from your OD limit to save on interest expenses and the unnecessary hassles for repayment. Prevent clauses where banks penalise underutilisation.

Summary

Borrowing through an overdraft is similar to borrowing a loan from a bank without the formalities and paperwork. Bank accounts may come with pre-entitled credit limits, or you can avail of the facility by applying with your bank or lender.

An overdraft facility provides businesses with immediate liquidity and cash flow management to meet short-term expenses cost-effectively. However, you should use ODs responsibly to ensure you remain in good financial standing with an appropriate credit rating.

Get international bank accounts in 5 mins

Save as much as ₹10 lakh annually with Zero FX Margin

Real time payment tracking and instant FIRA

Get international bank accounts in 5 mins

Save as much as ₹10 lakh annually with Zero FX Margin

Real time payment tracking and instant FIRA

Frequently asked questions

Ans: A loan is better than an overdraft when you require an extensive credit amount over a longer period. Often, companies require huge funds to finance long-term business needs, such as buying land or updating technology. In that case, business loans are a better choice than ODs.

About the author

Finance

With extensive experience at Flipkart, ITC, and McKinsey, Rohit, our in-house Chartered Accountant now leads finance here at Skydo.

Verified by

CA Abhilove ShardaLatest blog posts

View all posts

Consignor vs Consignee: Meaning, Differences & Example

Top 5 Things to Keep in Mind When Hiring International Contractors (2026)

How Founders Actually Pay Global Contractors (2026)

Related blog posts

View all postsConsignor vs Consignee: Meaning, Differences & Example

Top 5 Things to Keep in Mind When Hiring International Contractors (2026)