Sole Proprietorship vs. Private Limited Company/Partnership/LLP

Whichever structure you pick, if you have international clients, Skydo gets you paid cleanly with FIRA on every payment.

“I am an entrepreneur, and I own a business”.

This statement has become common due to the ease of registering and operating businesses. However, the answers vary when you ask the type of business structure for their business.

An entrepreneur could also be a freelancer who wants to create a legally registered business and streamline all operations. For such a business, most people consider sole proprietorship for its simplicity in formation. It often involves minimal paperwork and costs, making it an attractive option for those starting a small business on a tight budget.

If you are currently a freelancer looking to legitimise your offerings through a business structure or considering a business idea, choosing a suitable structure is a critical success factor for your future business or company. It affects your enterprise’s revenue and profit potential in the long run, as explained further in this article.

While sole proprietorship is the simplest business structure, it may or may not be the most suitable for your business. You may ask–what other options do I have? How do I choose among them?

Understanding sole proprietorships vs. other business structures in detail through this blog will be key to answering these questions.

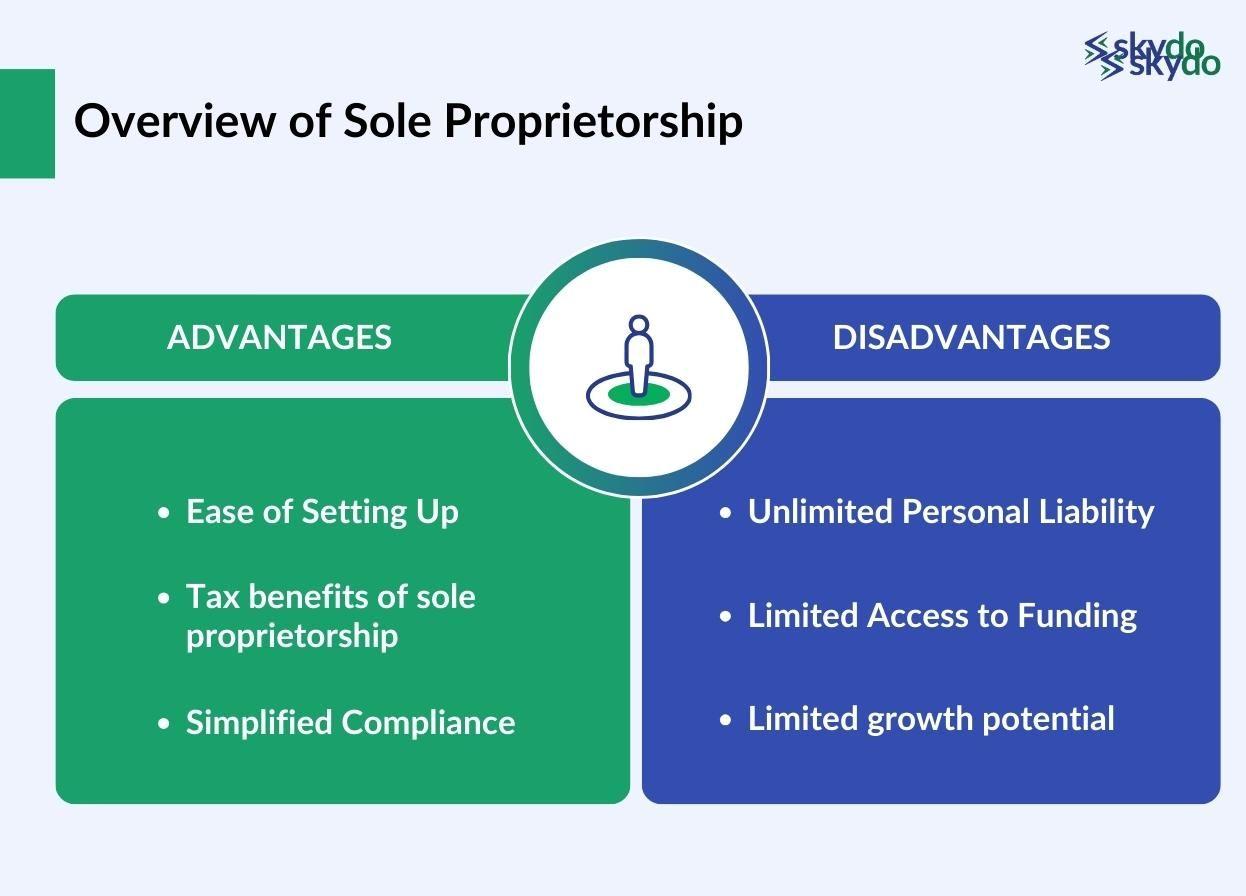

An Overview of Sole Proprietorship

a sole proprietorship is a business structure owned, managed and operated by a single individual.

Picture your local kirana shop owner who operates completely by themselves and is liable for managing the sales and the finances. A sole proprietorship is the simplest of all business structures, as the owner and the business entity are not considered separate from a legal and tax perspective.

Revenue Leak Calculator

- ✓ Fees quietly eating margin?

- ✓ Current provider vs Skydo

- ✓ Reclaim what's yours

Advantages of Sole Proprietorship

- Ease of Setting Up: Setting up a sole proprietorship is straightforward and involves minimal legal formalities. The registration process is extremely simple, with limited paperwork and quick approval. Furthermore, the sole proprietorship is not subject to extensive regulatory compliances as opposed to a private limited or partnership structure.

- Tax benefits of sole proprietorship: One of the biggest advantages of a sole proprietorship is that the business is seen as one with the owner legally. This means that the business's profits and losses are reported on the owner's tax return. The owner doesn't have to file separate taxes for the business.

- Simplified Compliance: Unlike larger business structures, sole proprietorships have minimal ongoing compliance obligations. This simplicity extends to periodic filings, reducing administrative burden compared to companies that must adhere to annual and quarterly filing requirements with authorities such as the MCA.

Disadvantages of Sole Proprietorship

Although this simple business structure comes with a host of advantages, it is not without certain disadvantages.

- Unlimited Personal Liability: This factor makes the owner liable to cover the debt through their assets, such as family home or personal savings, if the business cannot meet its financial obligations.

- Limited Access to Funding: Banks and financial institutions are hesitant to provide personal or business loans to sole proprietors. Currently, there is no unified portal to access business documents similar to other business structures such as LLPs and companies where MCA has such documents available. The repayment also relies on the owner’s assets and creditworthiness.

Additionally, since there is no separate legal entity formed, the money can only be invested as debt, which has a lower return compared to equity, making it unattractive for funders.

- Limited growth potential:

Sole proprietorships face more challenges than other business structures to grow and expand because the owner is doing all the work single-handedly, with limited resources, and the limitation on taking on additional work.

Since the responsibility falls on a single owner who may not be skilled in every business aspect, it makes the growth potential for the business questionable.

Overview of Other Business Structures

Here are the most common alternative business structures to sole proprietorships.

Partnerships

This type of business structure involves two or more individuals who come together to form a legal business entity. The partners create a partnership deed, which details the profit or loss sharing ratio of each of them. They must also report the business income in their tax returns.

There are two types of partnerships.

- General partnerships: In a general partnership, a minimum of two and a maximum of twenty members come together to create a business. The partners in a general partnership have unlimited liability, with their assets considered to fulfil the firm’s financial obligations. General partnerships are registered under the Partnership Act of 1932.

- Limited Liability Partnerships: This structure is a separate legal entity from its partners, offering limited liability protection to its partners. In an LLP, partners' assets are not at risk in case of business debts or legal issues. The Limited Liability Partnership Act of 2008 governs LLPs in India.

Let’s consider a partnership example of "Smith & Johnson Law Firm."

John Smith and Sarah Johnson have come together to form a partnership for their law practice. They share ownership, responsibilities, and profits equally. However, it's important to note that in a general partnership like this, both partners have unlimited personal liability for the firm's debts and legal obligations. This means their assets could be at risk if the firm encounters financial difficulties.

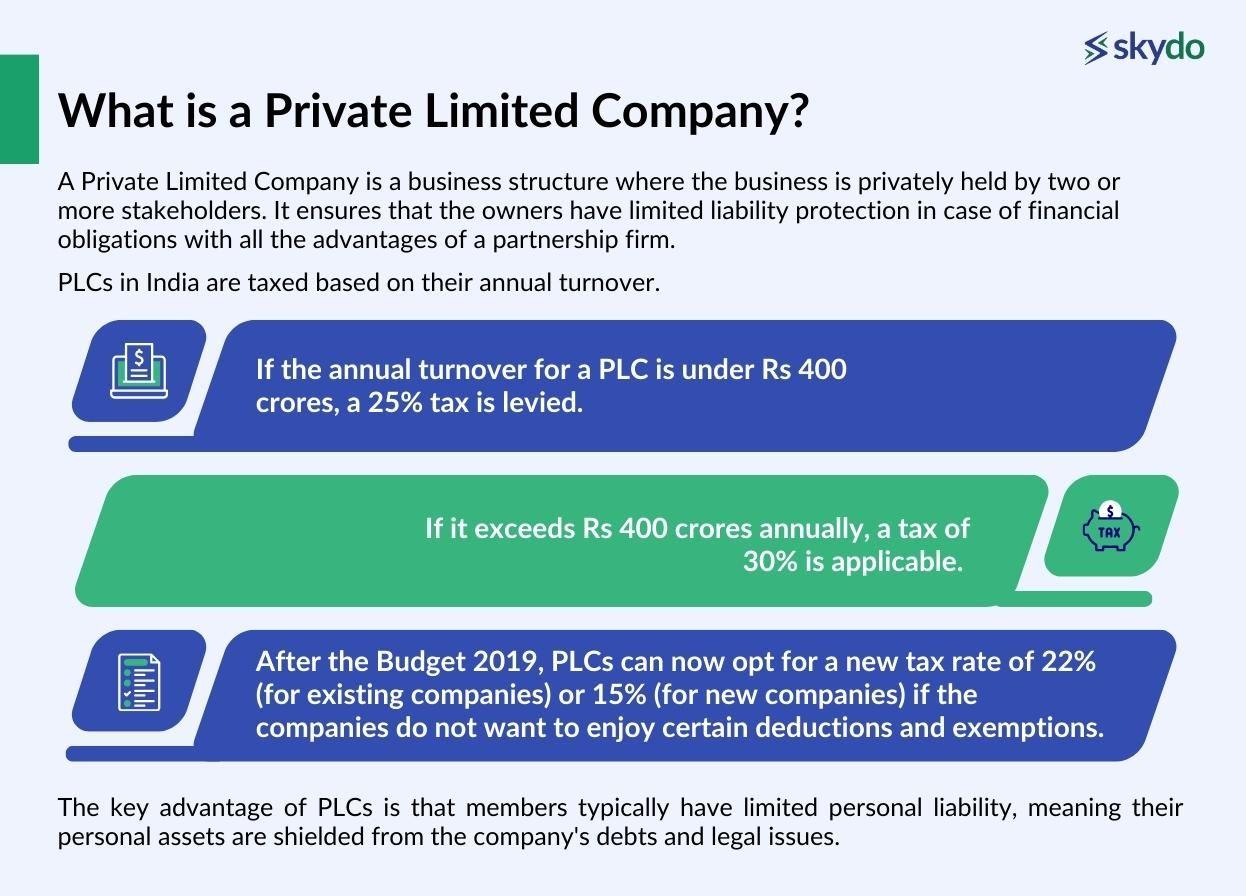

Private Limited Company (PLC)

A Private Limited Company is a business structure where the business is privately held by two or more stakeholders. It ensures that the owners have limited liability protection in case of financial obligations with all the advantages of a partnership firm. Being a separate legal entity, PLCs can enter into contracts, own assets, and incur debts in the company’s name.

PLCs in India are taxed based on their annual turnover. If the annual turnover for a PLC is under Rs 400 crores, a 25% tax is levied. If it exceeds Rs 400 crores annually, a tax of 30% is applicable. However, after the Budget 2019, PLCs can now opt for a new tax rate of 22% (for existing companies) or 15% (for new companies) if the companies do not want to enjoy certain deductions and exemptions.

The key advantage of PLCs is that members typically have limited personal liability, meaning their personal assets are shielded from the company's debts and legal issues. For example, ABC Tech Solutions PLC can choose its tax classification and management structure, offering versatility to adapt to its specific needs.

For example, ABC Tech Solutions PLC, a technology company, can choose its tax classification and management structure, offering versatility to adapt to its specific needs. Tax classification and management structures for a PLC could encompass options like the way you are taxed as a PLC, and determining management setups such as a board of directors or managerial hierarchy.

This allows its members to have limited personal liability, safeguarding their personal assets from the company's debts and legal issues.

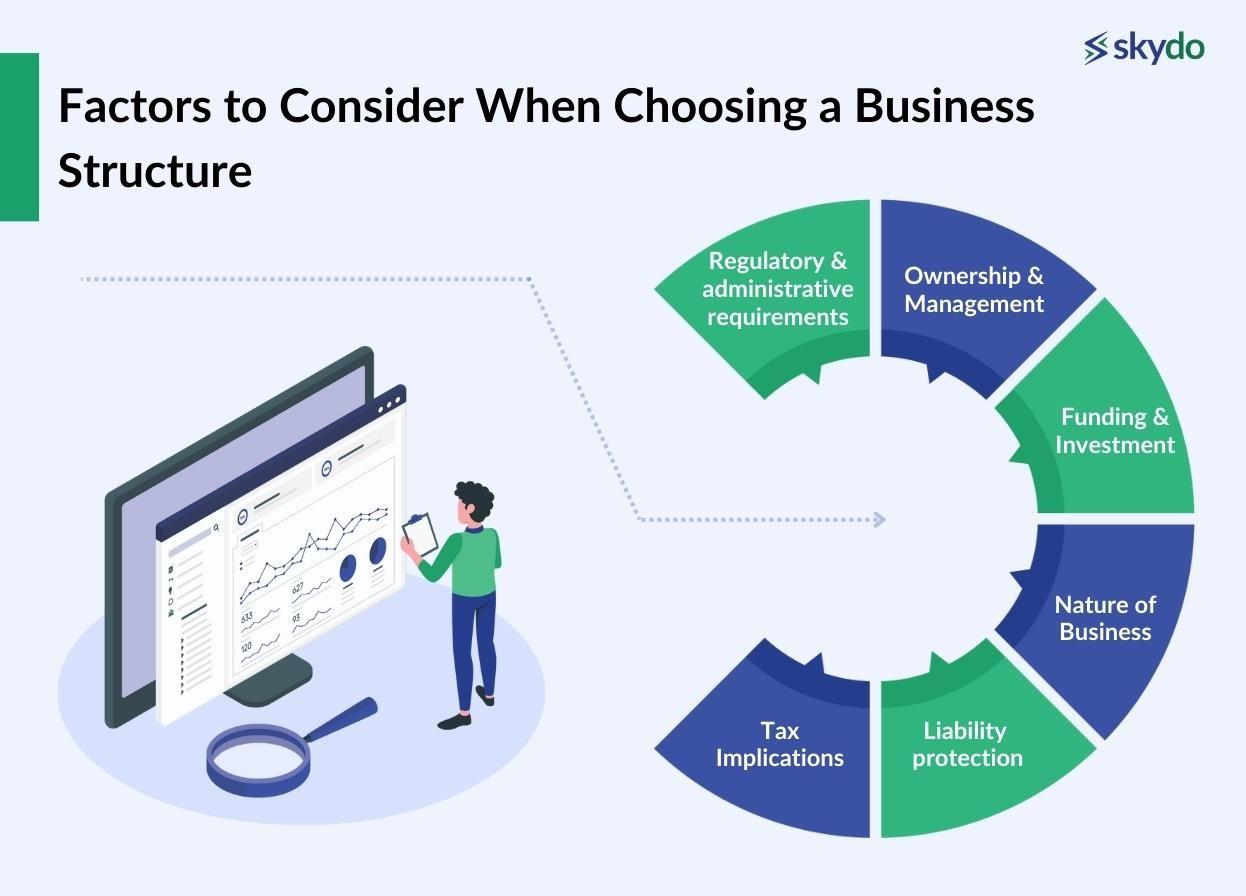

Factors to Consider When Choosing a Business Structure

Choosing a suitable business structure is vital for the success and sustainability of the business. Here are the factors you should consider when choosing a business structure.

1. Nature of Business

A sole proprietorship is ideal when the business is small and does not require extensive regulatory and tax-related compliance.

If your business requires the expertise or skills of two or more people but is smaller in scale, you may choose partnerships for better management.

A business with a larger scale than partnerships but limited offering can choose PLCs.

2. Liability protection

Sole proprietorships and general partnerships come with unlimited liability, while LLPs and PLCs come with limited liability. Based on the nature of the business and your personal risk tolerance, you can compare these business structures to determine your structural needs.

3. Tax Implications

Some structures, such as proprietorships and partnerships offer pass-through taxation, while structures such as PLCs may force you to pay both corporate or personal tax.

Navigating corporate taxes can increase the complexity of tax compliance, and you should decide based on your convenience for each structure’s taxation requirements.

4. Ownership and Management

Before choosing a business structure, you should decide the level of control ownership you want over business decisions and management.

Sole proprietorships and partnerships offer more control to the owners than PLCs, which may involve a democratic decision-making process based on mutual agreement.

5. Funding and Investment

Business structures such as sole proprietorships face difficulties in raising external capital, making them less suitable for entrepreneurs seeking funding as opposed to private limited companies that can issue shares of stock to raise funds.

6. Regulatory and administrative requirements

Sole proprietorships and partnerships have the simplest compliance requirements, usually limited to basic tax filings. PLCs have higher regulatory and administrative compliance when compared to sole proprietorships and partnerships.

Decision-Making Process For Your Business

You’ve got the business idea, and it’s entirely up to you to decide how you want to convert it into reality. However, achieving business goals is based on their effective identification. Before you choose a business structure, you must analyse and assess the business goals extensively.

Ask yourself questions such as:

- Why are you creating the business?

- What amount of profit do you want to generate from the business annually?

- How many products or services do you want to sell or offer in a specific time frame?

Once you have set your business goals, consider the following key steps to evaluate the business structure options.

- Liability Tolerance: Determine if your assets or savings allow you to choose a business structure with unlimited liability comfortably. If you feel your liability tolerance is low, choose a business structure with limited liability.

- Tax Implications: If you want to enjoy pass-through taxation benefits, choose the business structure that provides reporting business income in personal taxes. However, if you want your business to be a separate legal identity, you can choose a structure without pass-through taxation benefits.

- Ownership Preferences: If you want complete control, you may opt for sole proprietorship. In case your ideal ownership level is partial, you may consider partnerships or PLCs.

- Funding and growth opportunities: You may choose a business structure to which banks and financial institutions give loans easily rather than business structures such as sole proprietorships that face credit difficulties.

- Administrative requirements: You can evaluate different business structures based on your expertise and skills in regulatory and administrative compliance. It will ensure effective adherence and compliance and the continued legality of your business.

Conclusion

Every business structure comes with its own set of advantages and disadvantages, and the choice to evaluate all and choose one depends entirely on your business’s future goals and needs.

Since business structures are the backbone of the entire business and come with specific regulations and taxation requirements, it is wise to consult a Chartered Accountant and a business advisor for a better structural approach. In today’s digital age, you can also use Ask AI help to get instant, data-driven insights into different business structures based on your inputs—such as industry type, investment capacity, risk appetite, and long-term vision. AI-powered tools can help you compare structures like sole proprietorship, partnership, LLC, and corporation by outlining pros, cons, tax implications, and scalability options. While not a substitute for professional legal advice, asking AI can give you a head start in understanding your options before consulting an expert.

Remember that the choice of business structure is not fixed and can be changed as your business evolves. However, making an informed decision from the start can save you time, money, and potential complications down the road.

Get international bank accounts in 5 mins

Save as much as ₹10 lakh annually with Zero FX Margin

Real time payment tracking and instant FIRA

Get international bank accounts in 5 mins

Save as much as ₹10 lakh annually with Zero FX Margin

Real time payment tracking and instant FIRA

Frequently asked questions

Ans: If you want to obtain funding to start a business, there are several options available to you, such as–

- Using your personal savings

- Taking out loans from banks or credit unions

- Seeking investment from friends and family

- Exploring angel investors or venture capitalists

- Launching crowdfunding campaigns

- Applying for small business grants

Click here to read more about the legal and regulatory steps for starting a sole proprietorship.

It's important to create a well-crafted business plan that outlines your strategy and financial projections to attract potential investors or lenders.

About the author

Legal & Compliance

“Love working with the best bunch of enthu-cutlets to create a great product”

Verified by

CA Abhilove ShardaLatest blog posts

View all posts

Consignor vs Consignee: Meaning, Differences & Example

Top 5 Things to Keep in Mind When Hiring International Contractors (2026)

How Founders Actually Pay Global Contractors (2026)

Related blog posts

View all posts

Current vs Savings Account for Freelancers in India

Upwork Payment Methods: How to Withdraw Payment from Upwork